What This Means to Distributors: Demand is still growing, but distributors should prepare for more price pressure, longer lead times and cautious customer ordering as supply chain volatility rises.

U.S. manufacturing expanded for a third straight month in March, but the latest Institute for Supply Management report showed growth was accompanied by rising costs, slower supplier deliveries, and continued caution on hiring.

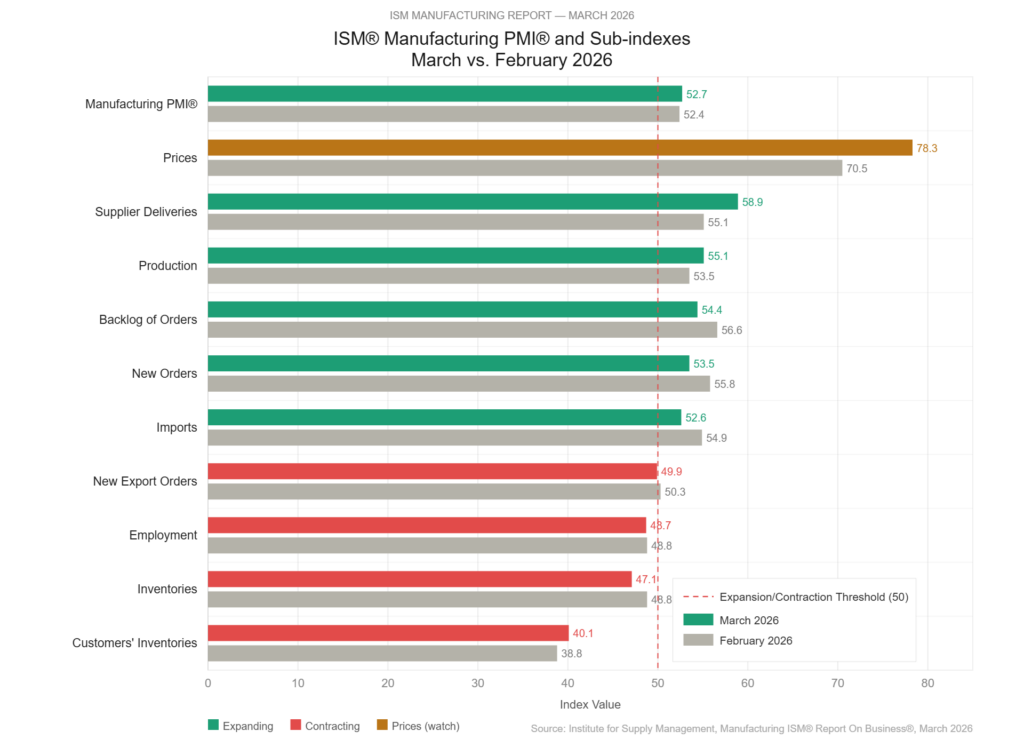

ISM said its Manufacturing PMI rose to 52.7 in March from 52.4 in February. A reading above 50 indicates expansion. New orders and production stayed in growth territory, while employment and inventories remained in contraction.

The report suggests factory demand is holding up, but operating conditions are getting tougher. ISM’s prices index jumped to 78.3 from 70.5 in February, its highest level since June 2022. The supplier deliveries index rose to 58.9 from 55.1, indicating longer lead times.

Susan Spence, chair of ISM’s Manufacturing Business Survey Committee, said manufacturing “remained in expansion territory” in March and grew “at a slightly faster pace than the month before.”

At the same time, she said survey respondents pointed to mounting disruption tied to tariffs and the war in the Middle East.

“This month also marks the first report with panelists citing the Iran war as a new impact to their business, along with ongoing uncertainty with U.S. economic policy,” Spence said. She added that 64% of respondents’ comments were negative, with about 20% citing tariffs and about 40% citing the war in the Middle East.

New orders, a key measure of demand, fell 2.3 points to 53.5, though they remained in expansion for a third straight month. Production increased to 55.1 from 53.5. Backlogs also stayed in growth territory at 54.4, though that was down from 56.6 in February.

Employment remained weak. ISM’s employment index edged down to 48.7 from 48.8, extending a long stretch of contraction. Spence said 55% of panelists reported that managing head count, rather than hiring, remains the norm.

Inventories also contracted, with that index falling to 47.1 from 48.8. At the same time, the customers’ inventories index rose to 40.1 from 38.8 but remained in “too low” territory, a sign that customers may need to rebuild stock if demand continues.

Exports weakened in March. ISM’s new export orders index slipped to 49.9 from 50.3, returning to contraction. Imports remained in growth territory at 52.6, though that was down from 54.9 in February.

Among the 18 industries tracked by ISM, 13 reported growth in March. The industries reporting expansion included transportation equipment, computer and electronic products, machinery, chemical products, fabricated metal products, and wood products. Three industries contracted: plastics and rubber products; furniture and related products; and food, beverage, and tobacco products.

Survey comments pointed to broad concern over higher energy and materials costs, supply chain disruption, and geopolitical risk. Respondents in transportation equipment, food manufacturing, chemicals, and plastics said the conflict in the Middle East was already affecting lead times, shipping, and input costs.

ISM said the March PMI reading is consistent with a 1.8% annualized increase in real gross domestic product. The overall economy has now expanded for 17 straight months, based on ISM’s historical comparisons.

For manufacturers, March brought another month of growth. But it also brought clearer signs that production is becoming more expensive and less predictable.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: