Why This Matters to Distributors: Demand is stabilizing, but rising costs, slower deliveries and ongoing labor cuts point to continued margin pressure. Distributors should expect more price increases, cautious customer ordering and uneven demand tied to geopolitical risk.

U.S. manufacturing activity expanded for a fourth straight month in April, but the pace of growth showed signs of strain as input costs climbed sharply and hiring continued to decline, according to the latest report from the Institute for Supply Management.

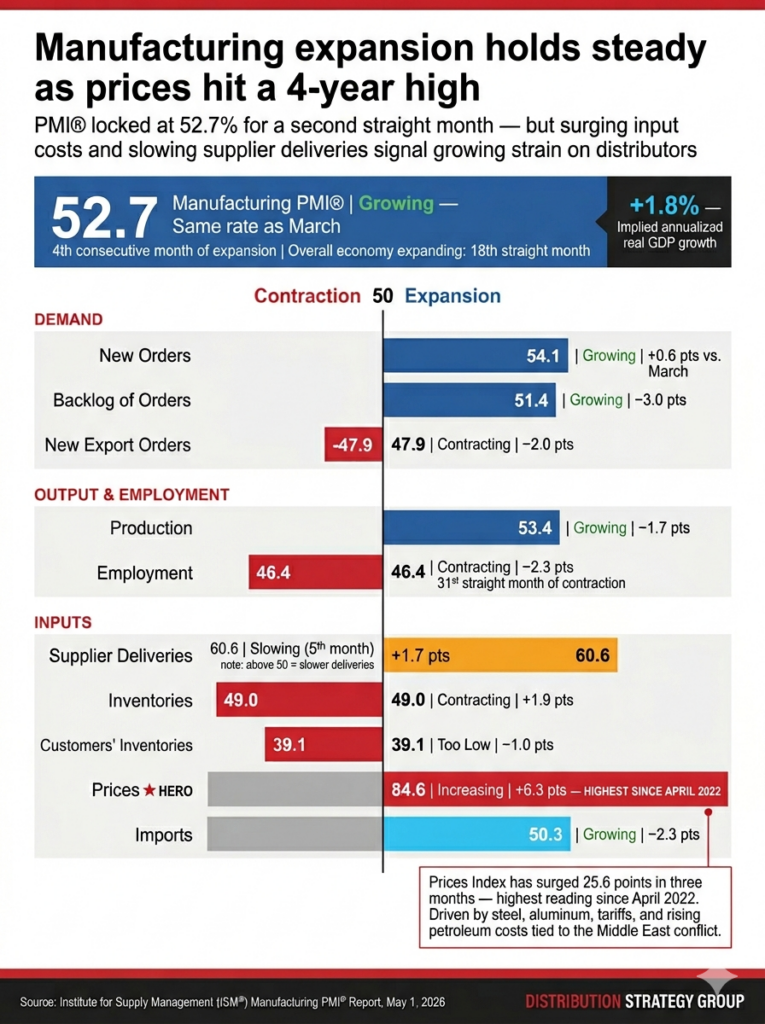

The ISM Manufacturing PMI registered 52.7% in April, unchanged from March and above the 50% level that indicates expansion. The reading suggests the broader economy continued to grow, extending an 18-month expansion streak.

Demand improved modestly. The New Orders Index rose to 54.1%, its fourth consecutive month of expansion. Production remained in growth territory but slowed, with the Production Index declining to 53.4% from 55.1% in March.

Cost pressures accelerated sharply. The Prices Index increased 6.3 percentage points to 84.6%, the highest level since April 2022. Over the past three months, the index has climbed more than 25 points, reflecting broad-based increases in metals, energy, and transportation costs.

Supply chain conditions tightened as delivery times lengthened. The Supplier Deliveries Index rose to 60.6%, indicating slower deliveries for the fifth consecutive month.

Labor conditions continued to weaken. The Employment Index fell to 46.4%, marking its 31st straight month of contraction. Survey respondents said companies are managing headcount primarily through attrition and selective layoffs rather than hiring.

Inventory data suggests a potential near-term boost to production. The Customers’ Inventories Index dropped to 39.1%, indicating stock levels remain too low and could support future orders. At the same time, manufacturers’ own inventories remained in contraction.

Trade activity weakened amid global uncertainty. The New Export Orders Index fell further into contraction to 47.9%, while the Imports Index declined to 50.3% but remained slightly in expansion.

Survey respondents pointed to geopolitical instability and trade policy as key concerns. The ongoing conflict involving Iran and continued tariff volatility were cited as drivers of higher costs and supply chain disruption.

“Demand for manufactured goods is trending higher versus last year. However, geopolitical uncertainty and rising oil and diesel prices continue to weigh on demand,” one transportation equipment executive said.

Another respondent said imports from China have increased 15% to 25%, driven by higher energy costs and tariffs, creating challenges in passing through price increases.

Among the largest manufacturing industries, transportation equipment, machinery, computer and electronic products and chemical products reported growth in April.

The report shows a manufacturing sector that continues to expand but is facing mounting pressure from inflation, geopolitical risk and labor constraints, conditions that are likely to keep pricing, inventory management, and supply chain strategy at the center of distributor decision making in the months ahead.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: