Why This Matters to Distributors: Artificial intelligence has become one of wholesale distribution’s highest strategic priorities, yet most companies remain stuck in pilot projects. Distribution Strategy Group’s inaugural AI Top 25 identifies the distributors that have successfully deployed AI at scale, offering the industry’s first evidence-based benchmark for measuring AI maturity and revealing what separates the leaders from everyone else.

Artificial intelligence has become wholesale distribution’s favorite technology topic.

It dominates conference agendas. It has become a recurring subject on earnings calls and in boardroom meetings. Every major distributor now describes AI as a strategic priority, while technology providers promise a new generation of tools capable of transforming everything from pricing and product search to customer service, inventory management, and warehouse operations.

But amid the surge of announcements, pilot programs, and vendor partnerships, one question remained unanswered:

Which distributors have turned AI into a competitive advantage?

Distribution Strategy Group set out to answer that question with what it describes as the first evidence-based benchmark of AI maturity in wholesale distribution.

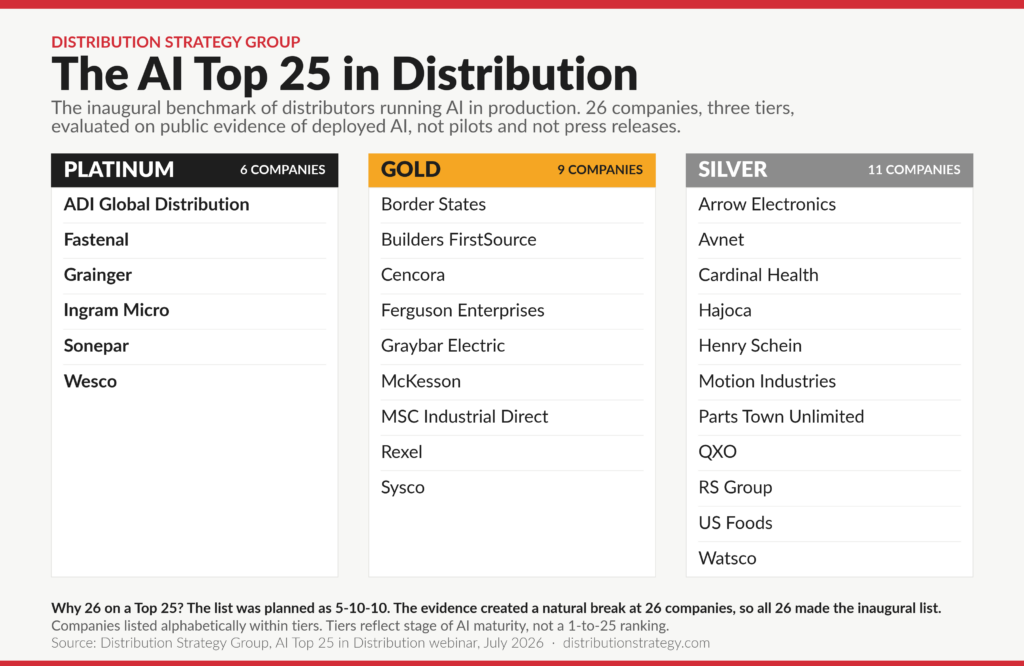

After evaluating more than 300 North American distributors over two years, researchers identified just 26 companies with verified AI deployments operating in production. The result is the inaugural AI Top 25, a benchmark that distinguishes companies generating measurable business results from those still experimenting with pilots, proofs of concept or announced initiatives.

The findings suggest the distribution industry has entered a new competitive phase.

While most distributors are still determining where AI fits within their organizations, a small group has moved beyond experimentation. Those companies have spent years modernizing enterprise systems, improving data quality, and embedding AI into sales, pricing, customer service, warehouse operations, and finance. For them, AI is no longer a technology initiative. It is becoming part of the operating model.

“The industry needed a credible, evidence-based benchmark,” DSG chief operating officer Brian Hopkins said during the July 14 webcast announcing the rankings. “There is a lot of noise around AI. We wanted to identify what is actually running in production inside distribution companies.”

That distinction shaped every aspect of the research.

Roadmaps were excluded. Press releases did not qualify. Technology partnerships and pilot projects also were excluded. Only production deployments supported by verifiable evidence counted toward the rankings.

A Much Smaller Group Than Expected

The report’s most striking finding wasn’t which companies made the list.

It was how few did.

DSG’s State of AI in Distribution 2026 survey found that 93% of distributors consider AI a strategic priority, yet only 16% have progressed beyond pilots into production deployments. The survey, which included 233 distributors, found the industry remains caught between ambition and execution.

Two-thirds of distributors remain in the exploration or pilot stage. About half either lack formal AI governance or are unsure whether one exists, while one in five has no formal process for measuring the return on investment from AI initiatives.

“What we mean by this gap is that companies are convinced AI matters,” DSG co-founder and managing partner Jonathan Bein said. “But they’re still in pilots or conceptual stages rather than execution. We believe that gap will narrow over the next several years because many of today’s pilots will eventually become production deployments.”

The research also challenges one of the industry’s biggest assumptions. Technology is no longer the principal obstacle because people are.

“The number one barrier is people, not technology,” Bein said. “Either people don’t have the skills or they’re skeptical about AI. We’ve watched that skepticism begin to change over our last four Applied AI conferences as fear turns into excitement.”

That observation helps explain why the companies at the top of the rankings differ so sharply from those still struggling to gain traction. The leaders did not simply purchase AI software. They changed how their organizations operate.

Six Companies Set the Standard

Only six distributors earned DSG’s highest recognition.

Rather than assigning numerical rankings, DSG grouped companies into Platinum, Gold, and Silver tiers, concluding that publicly available evidence could distinguish levels of AI maturity but could not credibly determine whether one company deserved to rank seventh instead of eighth.

The Platinum tier includes:

- ADI Global Distribution

- Fastenal

- Ingram Micro

- Sonepar

- W.W. Grainger

- Wesco International

The six companies have little in common. They operate in different markets, serve different customer bases, and have different ownership structures. Some embraced digital commerce years ago, while others accelerated more recently. Some built their AI capabilities around customer-facing applications, while others focused first on operations.

“What surprised me was the spread of the type of company,” Hopkins said. “They’re not all huge industrial distributors. They’re different types with a similar path to AI.”

That shared path, and not any single technology, separated the Platinum companies from the rest of the field.

Researchers found each embedded AI into the operating model rather than treating it as a stand-alone technology initiative. Each expanded beyond isolated use cases into multiple business functions. And each measured AI success through business outcomes rather than technology milestones.

Six Different Strategies, One Destination

Although the Platinum companies arrived at AI leadership through different paths, they reached remarkably similar conclusions about how the technology creates competitive advantage.

No company better illustrates AI’s ability to reshape commercial operations than ADI Global Distribution.

Rather than deploying isolated AI applications, ADI integrated artificial intelligence across product search, pricing, and order processing, creating a commercial workflow in which each stage of the buying process becomes increasingly automated and data driven.

DSG’s research found that approximately 1,700 customer orders enter the business each day without human intervention. AI also supports dynamic pricing, while 44% of customers purchase through digital channels. Together, those capabilities create a commercial engine in which search informs pricing, pricing accelerates transactions and automation reduces manual work.

“Most distributors, if they’ve got AI at all, are running one of those things,” Hopkins said. “They’ve managed to go through all three in one process.”

That integration, rather than any single application, distinguishes ADI. AI is no longer supporting the sales process. It is becoming part of how the company sells.

Fastenal followed a very different strategy, embedding AI inside customer facilities rather than concentrating it within its own operations.

Its network of more than 136,000 connected vending and bin-stock devices monitors inventory consumption, predicts replenishment requirements, and automatically initiates reorders, while robotics support operations in 15 distribution centers. According to DSG’s research, those connected devices account for 62% of Fastenal’s sales.

“It’s living where the customer lives,” Hopkins said. “That’s where it starts to make you embedded with the customer.”

The strategy extends beyond automation. Every connected device strengthens Fastenal’s relationship with customers by embedding the distributor directly into inventory management. Competitors are no longer replacing only a supplier. They are replacing an intelligent inventory management system integrated into the customer’s daily operations.

Ingram Micro rebuilt digital commerce around AI.

Rather than adding AI capabilities to an existing ecommerce platform, the technology distributor redesigned digital commerce around Xvantage, an AI-powered platform that recommends products, generates quotes, and improves order conversion. DSG’s research found Xvantage produced more than 100,000 AI-assisted order conversions during 2025, while agentic AI has operated in production since October.

“They didn’t take an AI tool and bolt it onto their current process,” Hopkins said. “They actually built a new platform.”

The decision reflects a broader pattern among AI leaders. Rather than layering new technology onto legacy systems, they are redesigning core business processes around artificial intelligence.

The Blueprint Behind the Leaders

The six Platinum distributors reached the top of DSG’s AI benchmark through very different strategies. Some focused first on customer-facing applications, while others concentrated on pricing, warehouse automation, or finance. Some built AI around digital commerce, while others embedded it in inventory management or back-office operations.

Despite those differences, researchers found they followed a remarkably similar path. Artificial intelligence was never treated as a stand-alone technology initiative. Instead, it became part of the operating model, influencing how decisions were made, how employees worked and how customers interacted with the business. That distinction, more than any individual technology deployment, separated the industry’s leaders from companies still experimenting with AI.

“We’re not looking at six companies running the same software,” Hopkins said during the webcast. “We’re looking at six companies that figured out how to make AI part of the business.”

After evaluating more than 300 distributors, DSG researchers identified five characteristics that consistently distinguished AI leaders from the rest of the industry.

Leadership Came Before Technology

Every distributor earning a place in the AI Top 25 assigned clear executive ownership for AI. Responsibility didn’t rest with committees, innovation councils, or loosely organized technology teams. It belonged to one executive with the authority to make decisions, allocate resources and drive adoption across the enterprise.

“All these folks named a single owner,” Hopkins said. “If you have budget authority, you’re the owner. You’re not a committee.”

Researchers found that organizational clarity mattered as much as technical capability. Companies struggling to scale AI often struggled because accountability was fragmented across multiple departments rather than concentrated in a single leader responsible for execution.

Production Mattered More Than Pilots

The benchmark deliberately ignored AI pilots, partnership announcements, and technology demonstrations. Only production deployments counted, immediately separating companies experimenting with AI from organizations already depending on it to run their businesses.

“They stopped piloting a couple years ago and started making sure it worked across the business,” Hopkins said.

That distinction fundamentally changes how companies think about AI. A pilot evaluates technology. Production changes how work gets done. The companies in the Platinum tier had already crossed that line, making AI part of everyday operations rather than a limited proof of concept.

AI Expanded Across the Enterprise

Most distributors begin with a single use case, whether it’s product search, pricing, customer service, or demand forecasting. The Platinum companies rarely stopped after the first success. Instead, they connected one deployment to the next, creating systems in which AI applications reinforced one another.

Search improved pricing. Pricing accelerated quoting. Quoting reduced manual order entry. Warehouse automation improved forecasting, while customer interactions generated better data that strengthened future AI models.

“The companies that started this process are now taking multiple AI use cases and putting them together simultaneously,” Hopkins said. “That’s going to be a differentiator over the next couple years.”

Researchers repeatedly observed that the competitive advantage came less from individual applications than from the way those applications worked together.

AI Became a Multiyear Strategy

None of the Platinum companies approached AI as an annual technology initiative. Instead, they invested over several years, modernizing enterprise systems, improving data quality, and building organizational capabilities before expanding AI across the business.

“They’re taking big swings,” Hopkins said. “It’s not a one-time investment this year. It’s investment over a number of years.”

That patience helps explain one of the report’s most important findings. Most of the Platinum companies began building AI capabilities years before ChatGPT introduced generative AI into the mainstream, giving them a significant head start over much of the industry.

Every Deployment Solved a Business Problem

The technologies varied widely, but researchers found one common thread across every company in the AI Top 25. Each deployment was tied directly to a measurable business outcome rather than a technology milestone.

Some companies focused on reducing inventory. Others measured order conversion, customer adoption, invoice automation, revenue growth, or productivity improvements. The metrics differed, but every AI initiative was evaluated against business performance rather than technical achievement.

“They’ve tied it to a number,” Hopkins said. “They’ve quantified the outcomes they expect.”

Gold Tier: The Next Wave of Leaders

If the Platinum tier represents the industry’s current AI leaders, the Gold tier illustrates how quickly the competitive landscape is changing. The nine Gold companies—Border States, Builders FirstSource, Cencora, Ferguson Enterprises, Graybar, McKesson, MSC Industrial Direct, Rexel USA and Sysco—have all embedded AI into meaningful business processes and demonstrated measurable results. What separates them from Platinum is not the sophistication of the technology but the breadth of deployment across the enterprise.

“Several of these are on the edge,” Hopkins said during the webcast. “They very clearly can make the Platinum stage next year.”

Each company demonstrates a different path toward AI maturity. Border States showed that employee ownership is no barrier to innovation, using AI-driven demand forecasting to reduce inventory while producing measurable financial returns. Sysco demonstrated that successful AI adoption depends as much on organizational change as software by integrating AI directly into the daily workflow of its sales force. Cencora distinguished itself through sustained investment, while McKesson continued expanding robotics and intelligent warehouse automation. Graybar, Ferguson, MSC Industrial Direct, Rexel USA and Builders FirstSource each demonstrated that AI leadership is spreading rapidly across electrical, industrial and construction distribution.

Together, the Gold companies suggest the gap separating today’s leaders from tomorrow’s leaders is narrowing rapidly.

Silver Signals the Industry’s Next Wave

The 11 Silver companies reinforce another important conclusion from the research: meaningful AI adoption is no longer confined to the industry’s largest or most digitally advanced distributors. Arrow Electronics, Avnet, Cardinal Health, Hajoca, Henry Schein, Motion Industries, Parts Town Unlimited, QXO, RS Group, US Foods, and Watsco all demonstrated verified production deployments that met DSG’s evidence standard.

“They’re not beginners,” Hopkins said. “These are people who are actually making things happen.”

Collectively, the Silver tier shows that AI is spreading across every major distribution sector, including healthcare, industrial, HVAC, technology, foodservice and building products. For many of these companies, the challenge is no longer proving AI works. It’s determining how quickly they can scale successful deployments across the enterprise.

More Than a Ranking

The AI Top 25 says less about technology than it does about leadership. Researchers found that AI success had little correlation with ownership structure. Employee-owned companies, private-equity-backed firms, privately held distributors and public corporations all appear throughout the rankings. What mattered was leadership, disciplined execution, and a willingness to treat AI as a business transformation rather than another technology project.

The rankings will evolve as new technologies emerge and companies move between tiers. But DSG’s research points to a broader shift already underway. The distributors pulling ahead are no longer distinguished by whether they use artificial intelligence. They are distinguished by how deeply AI is woven into pricing, customer acquisition, warehouse operations, finance, and executive decision-making.

That is the real story behind the AI Top 25. It isn’t simply a list of companies using AI. It’s the first evidence that a new competitive model is taking shape in wholesale distribution, one in which artificial intelligence is becoming as fundamental to business performance as ERP systems, ecommerce and data analytics. The companies at the top are already operating in that future. The rest of the industry is racing to catch up.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: