Why This Matters to Distributors: For the 55% of distributors in the moderate-maturity tier, the DSG data makes a pointed argument: the technology budget problem is not what to buy next but whether the systems already purchased are actually connected — because a CRM that does not feed the ERP, an ecommerce platform not linked to live inventory, and an analytics stack training on incomplete data all produce the same outcome: technology spend without technology return.

Fifty-five percent of North American wholesale distributors have invested in core technology systems but have not integrated them — leaving customer relationship management data disconnected from analytics, e-commerce platforms unlinked from enterprise resource planning systems, and a significant portion of the industry sitting on sunk costs that have not yet paid off.

That finding anchors Distribution Strategy Group’s State of Distributor Technology 2026, a survey of 233 North American wholesale distribution executives conducted in Q1 2026. The report assessed 54 technology categories alongside artificial intelligence adoption patterns, governance structures, and self-assessed digital maturity, producing what DSG describes as the most granular picture yet of where the industry stands — not where it says it stands.

The headline finding is direct: digital maturity is the strongest predictor of technology return on investment. Not the tool a distributor buys. The organizational discipline builds around the tool. High-maturity distributors in the survey deploy an average of 28 technologies across the 54 assessed categories. Low-maturity peers average five. That gap does not close with a purchase order.

Three maturity profiles emerged from the data. High-maturity distributors, 29% of respondents, carry broad technology stacks, active AI programs, and governance structures. Low-maturity firms, 16% of respondents, operate basic systems with minimal AI activity and almost no formal governance. The moderate-maturity segment — 55% of respondents — is where DSG says strategic attention should concentrate. These distributors have the pieces. They have not built the platform.

The warehouse is the most consistent underinvestment in the survey. Half of all respondents use a warehouse management system (WMS). Radio frequency identification (RFID) adoption sits at 13%. AI-driven WMS adoption is below 2%. Forty-nine percent of respondents identified warehouse automation as a top AI use case — yet the foundational technology required to make AI-powered warehousing functional is absent. The gap cuts across every maturity segment, revenue tier, and sub-industry in the survey.

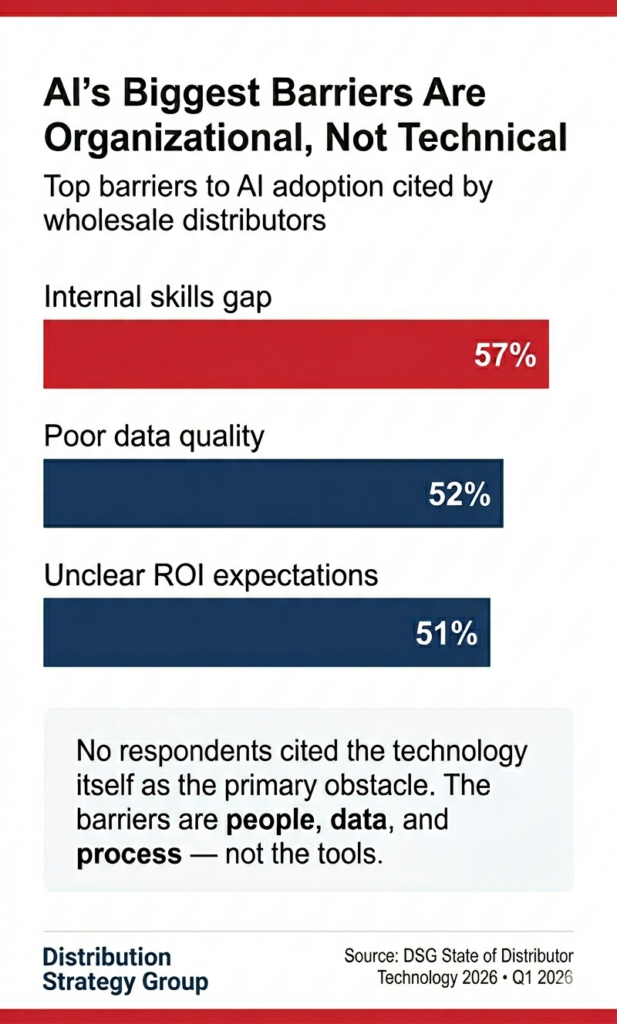

On artificial intelligence, the industry is enthusiastic and unprepared. Ninety-three percent of respondents are exploring AI or have moved beyond initial exploration. Only 23% have reached scaling or integration stage. The three largest barriers are organizational: skills gaps at 57% of respondents, poor data quality at 52% and unclear return on investment expectations at 51%. No respondents identified the technology itself as the primary obstacle.

The report also flags what it calls an ambition-execution mismatch affecting 18% of the industry. These distributors rate themselves as high maturity but deploy an average of fewer than seven technologies. Self-assessed maturity, the report concludes, is an unreliable foundation for technology strategy. Behavioral evidence — technology breadth, governance depth, integration reach — tells the real story.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: