Why This Matters to Distributors: Building materials distributors heading into the second half of 2026 face a cost structure running at its hottest pace in three years at the same moment the channel is consolidating around scaled national platforms with the purchasing power to absorb what independents cannot.

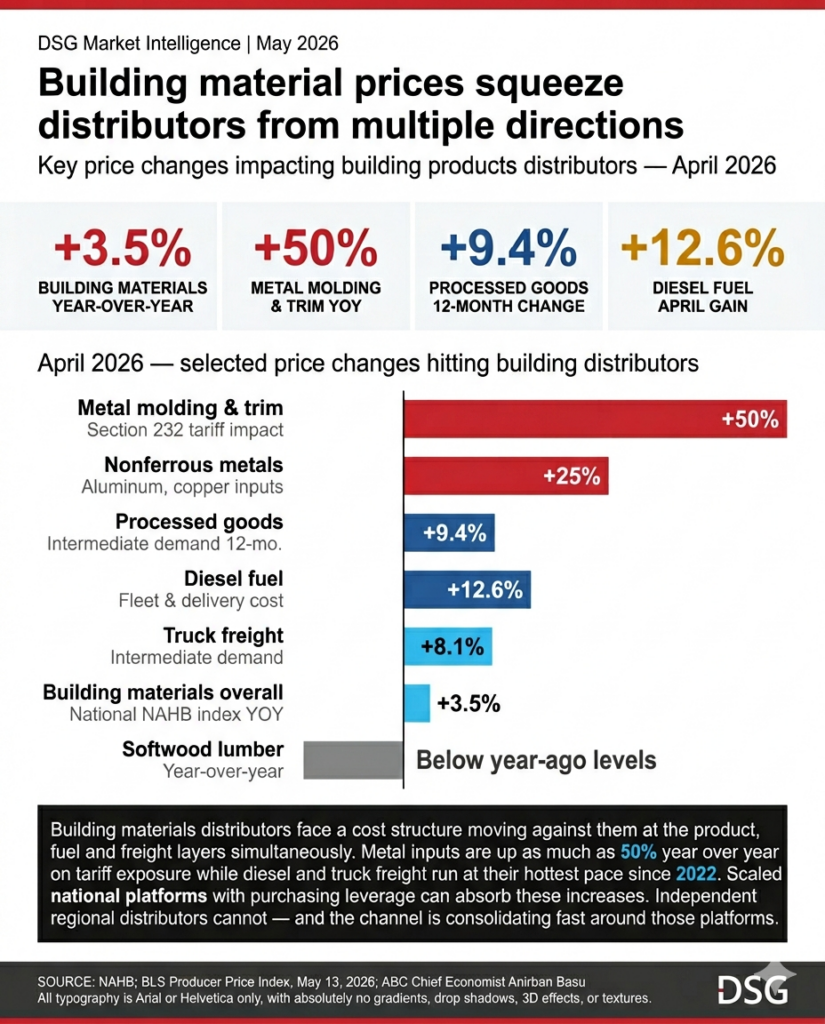

Building material prices rose 3.5% year over year through early 2026, the largest annual increase since early 2023, as tariff-driven metal costs, rising diesel prices and broader input inflation converged to compress margins across the building products supply chain, according to National Association of Home Builders data.

The price acceleration is uneven but broad. Metal molding and trim prices surged 50% compared to a year ago, reflecting the direct impact of Section 232 tariffs on steel and aluminum. Ready-mix concrete prices softened and softwood lumber prices remain below year-ago levels, but those pockets of relief have not offset the broader upward trend in materials costs heading into the second half of 2026.

The April Producer Price Index data from the Bureau of Labor Statistics reinforced the picture. Processed goods for intermediate demand rose 2.7% in April and are up 9.4% over the past 12 months, the largest such gain since October 2022. Diesel fuel jumped 12.6% in April in the intermediate demand pipeline. Truck freight costs rose 8.1% and transportation and warehousing services for intermediate demand climbed 3.7%.

The result is a cost structure moving against distributors at the product, fuel, and freight layers simultaneously. Associated Builders and Contractors chief economist Anirban Basu said the tariff environment makes it “exceptionally difficult to know how construction input prices will behave in 2026,” citing sharp escalation in aluminum mill shapes and primary and secondary nonferrous metals, both up more than 25% over the past year.

Demand dynamics vary sharply by segment, adding a second layer of pressure. Harvard Joint Center for Housing Studies projected homeowner renovation and repair spending at approximately $524 billion in early 2026, with growth moderating to around 2% through the year. Residential new construction remains rate sensitive. Commercial and institutional construction is carrying more of the load, driven by data centers, healthcare facilities, and office renovation. That divergence is creating uneven order flow for distributors whose customer bases skew toward one segment.

Building materials distribution generated more than $53 billion in monthly sales entering 2026, combining Census Bureau figures for building materials dealers and lumber and construction materials merchant wholesalers. That volume is moving through a channel under active consolidation pressure. QXO’s pending $17 billion acquisition of TopBuild, Home Depot’s SRS Distribution platform at more than 1,250 locations and Lowe’s $8.8 billion acquisition of Foundation Building Materials have repositioned the largest players with scale, geographic density, and category breadth that independent distributors cannot match.

The price environment compounds that competitive pressure. A regional distributor absorbing higher metals costs, higher diesel and higher freight while competing against a platform with the purchasing leverage to offset those same increases is operating at a structural disadvantage that widens as input costs rise. The ability to pass cost increases through to professional contractors managing tight project budgets on fixed-bid work has limits. Large-format distributors with diversified product portfolios and direct contractor relationships are better positioned to test those limits.

Lumber pricing remains one category where distributors have some relief. Softwood lumber prices are below year-ago levels and have not recovered to the post-pandemic peaks. That relief is narrowing, however, as tariff uncertainty around Canadian lumber imports introduces new pricing risk into the second half of 2026.

Basu said the unknown distribution of tariff costs through the supply chain is itself a planning obstacle, making it difficult for distributors to price forward contracts with confidence or commit to inventory levels that match uncertain demand.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: