Why This Matters to Distributors: Slower inventory investment, weakening corporate profits and stubborn inflation are creating mounting pressure on distributors heading into the second half of 2026, particularly in industrial, retail, and healthcare supply chains where customer demand is beginning to soften.

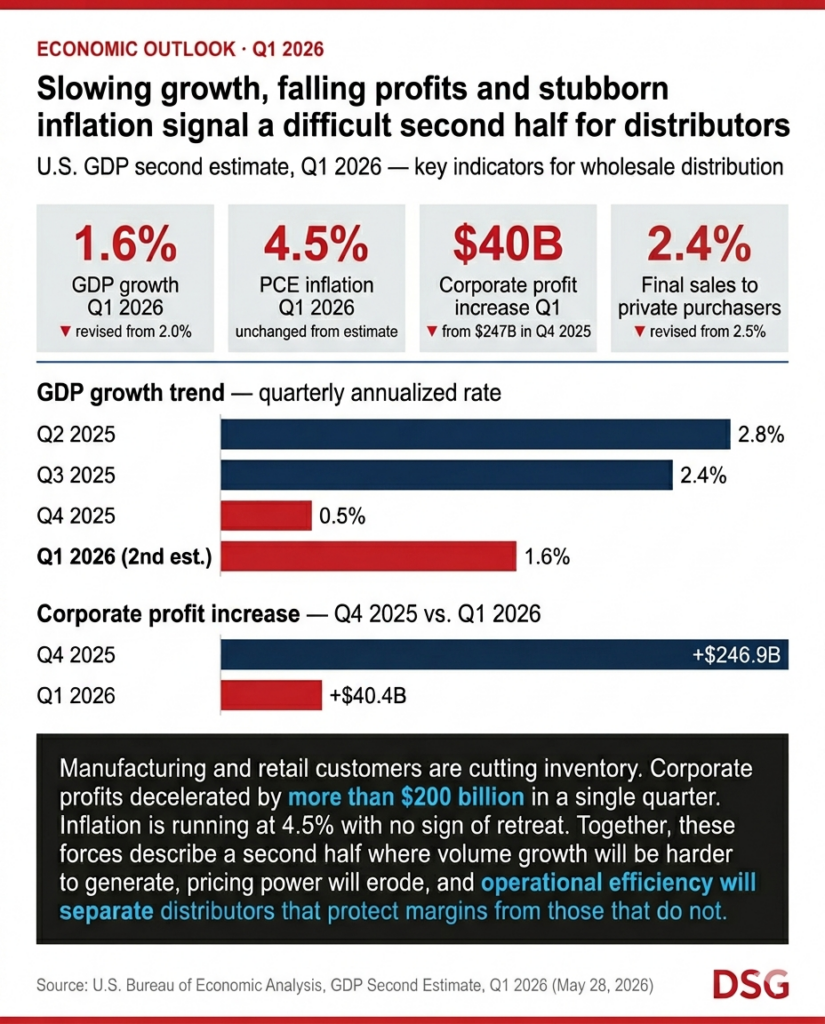

The U.S. economy grew at an annual rate of 1.6% in the first quarter of 2026, according to revised data released Thursday by the Bureau of Economic Analysis, down from the agency’s initial estimate of 2%.

The downward revision reflects weaker inventory investment and softer consumer spending, trends that could weigh heavily on wholesale distributors tied to manufacturing, retail, and healthcare markets.

The Bureau of Economic Analysis lowered its estimate for private nonfarm inventory investment, led by declines in manufacturing and retail trade activity. Inventory reductions in those sectors often translate into weaker replenishment demand for distributors.

Consumer spending on services also was revised lower, driven by reduced healthcare spending, including outpatient and hospital services. The changes could pressure medical surgeries and healthcare distributors whose sales volumes are linked to hospital and clinical activity.

Corporate profits also slowed sharply during the quarter. Profits from current production increased $40.4 billion in the first quarter, compared with a $246.9 billion increase in the fourth quarter of 2025.

The deceleration in profits could lead businesses to reduce capital spending, tighten procurement budgets, and place greater pricing pressure on distributors, particularly in industrial and business-to-business markets.

Inflation remained elevated during the quarter. The personal consumption expenditures price index, the Federal Reserve’s preferred inflation gauge, increased 4.5% in the first quarter. Excluding food and energy, the index rose 4.4%.

Persistent inflation continues to pressure distributors managing higher labor, transportation and product costs while facing increasing customer resistance to additional price increases.

Real final sales to private domestic purchasers, a measure of underlying domestic demand combining consumer spending and private investment, increased 2.4%, revised slightly lower from 2.5%.

The report does not point to a broad economic contraction, but it does suggest demand growth is slowing while inflationary pressures remain elevated.

The Bureau of Economic Analysis also noted that refunds tied to a February 2026 Supreme Court ruling involving certain tariffs imposed under the International Emergency Economic Powers Act were treated as capital transfers and therefore excluded from GDP calculations.

The agency will release its third estimate for first-quarter gross domestic product on June 25.

For distributors, the revised data reinforces concerns that the second half of 2026 could bring slower order growth, increased pricing pressure, and tighter customer spending across multiple end markets. Companies with stronger operational efficiency, inventory management and pricing discipline are likely to be better positioned if economic conditions continue to soften.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: