Why This Matters to Distributors: The latest manufacturing data points to a more volatile operating environment for distributors as stronger factory demand collides with rising costs, supplier delays and renewed inventory stockpiling tied to geopolitical disruption.

U.S. manufacturing activity accelerated in May to its strongest level in four years, but rising costs, slowing demand growth, and worsening supply chain disruptions are increasing pressure across industrial supply chains, according to new data from S&P Global.

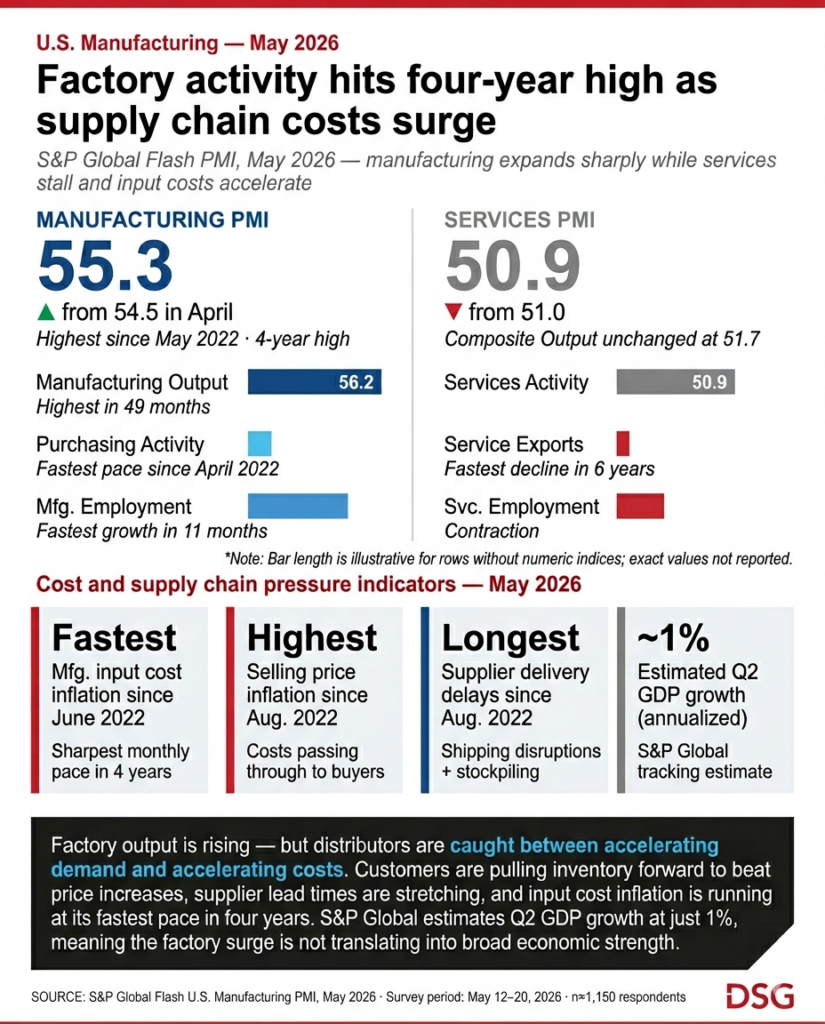

The S&P Global Flash U.S. Manufacturing Purchasing Managers’ Index rose to 55.3 in May from 54.5 in April, the highest reading since May 2022 and well above the 50 mark that signals expansion. Manufacturing output increased to 56.2 from 56.0, reaching its highest level in 49 months.

The gains in manufacturing contrasted with continued weakness in the service sector. The Flash U.S. Services PMI Business Activity Index slipped to 50.9 from 51.0 in April, while the broader Composite Output Index remained unchanged at 51.7.

S&P Global said manufacturers increased production and inventory levels partly because customers accelerated purchases and built precautionary inventory amid concerns about additional supply disruptions and future price increases linked to the ongoing war in the Middle East.

“The damaging economic impact from the war in the Middle East is becoming increasingly evident in the business surveys,” Chris Williamson, chief business economist at S&P Global Market Intelligence, said in the report.

Williamson said higher energy prices and supply chain disruptions are driving up costs while weakening demand and contributing to slower hiring activity across the broader economy.

Manufacturers reported the longest supplier delivery delays since August 2022 as shipping disruptions and inventory stockpiling strained supply chains. Factory purchasing activity increased at the fastest pace since April 2022 as companies expanded safety stock to guard against shortages and additional cost increases.

Input cost inflation accelerated sharply in May. Manufacturing input costs increased at the fastest monthly pace since June 2022, while overall selling price inflation climbed to its highest level since August 2022.

The report also showed diverging labor conditions between manufacturing and services companies. Manufacturing payrolls increased at the fastest rate in 11 months as factories added workers to support higher production levels. Service-sector employment, meanwhile, contracted at one of the sharpest rates since the pandemic period.

Despite the rebound in manufacturing activity, S&P Global said broader economic growth remains subdued. The firm estimated second-quarter gross domestic product growth is tracking at 1% annually as rising prices and geopolitical uncertainty continue to weigh on demand.

Export demand also remained weak across both sectors. Service exports declined at the fastest pace in six years, while manufacturers reported continued contraction in export orders even as domestic demand improved.

S&P Global collected survey responses between May 12 and May 20 from approximately 650 manufacturers and 500 service providers.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: