Why This Matters to Distributors: Manufacturing demand is strengthening across several of the largest distributor end markets, including machinery, fabricated metals and transportation equipment. However, higher material costs, slower supplier deliveries and ongoing component shortages are likely to keep pressure on pricing, inventory management and margins throughout the second half of 2026.

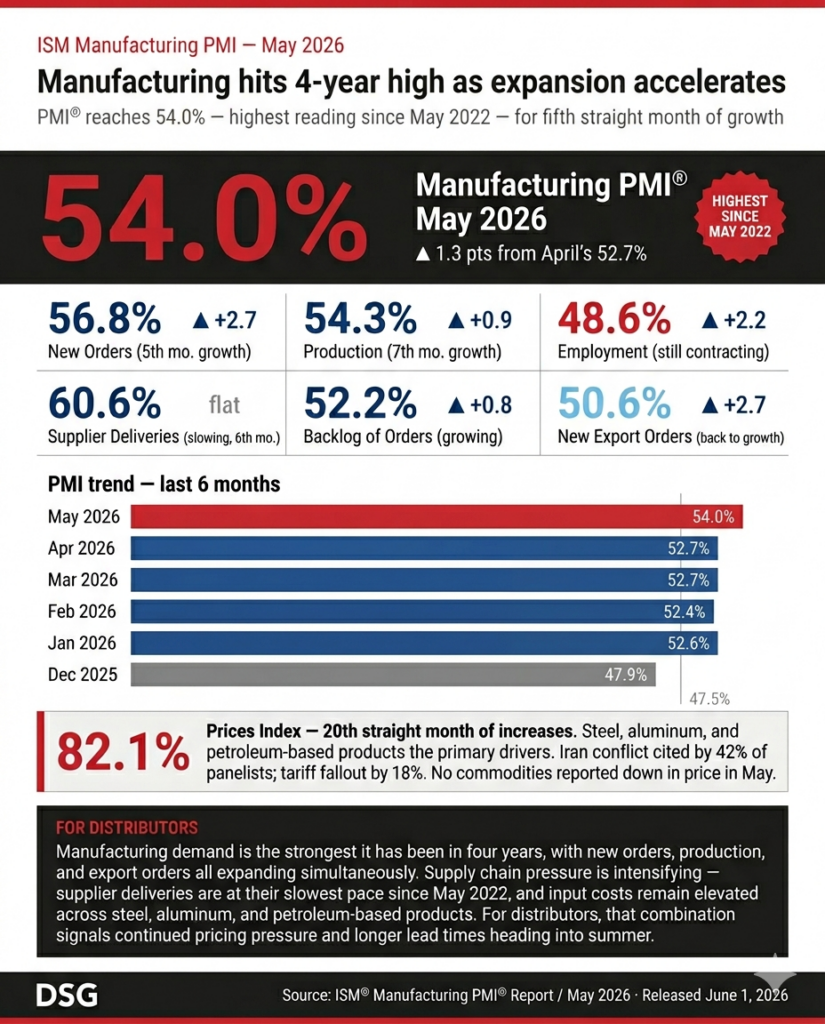

U.S. manufacturing activity expanded in May at its fastest pace in four years as new orders and production strengthened, offering an encouraging signal for distributors even as higher costs and supply chain disruptions continue to weigh on the sector.

The Institute for Supply Management’s Manufacturing PMI rose to 54.0 in May from 52.7 in April, marking the fifth consecutive month of expansion and the highest reading since May 2022. A reading above 50 indicates growth in manufacturing activity.

Demand continued to improve across much of the manufacturing economy. New orders increased to 56.8 from 54.1, while production rose to 54.3 from 53.4. Export orders returned to expansion territory, and order backlogs grew for a fifth consecutive month.

The gains were broad-based. Sixteen of 18 manufacturing industries reported growth in May, including machinery, fabricated metal products, transportation equipment, chemical products and computer and electronic products. Those sectors account for a significant share of demand for industrial, MRO, electrical and specialty distributors.

At the same time, manufacturers continued to report mounting cost pressures.

The ISM Prices Index registered 82.1, indicating raw material prices increased for a 20th consecutive month. Survey respondents cited rising steel and aluminum prices, higher petroleum-related costs and the lingering effects of tariffs on imported goods as major contributors to inflation.

Many manufacturers also pointed to growing uncertainty tied to conflict in the Middle East. Respondents reported rising fuel costs, supply disruptions and concerns about long-term availability of key materials. Several cited shortages of semiconductors, electronic components, tungsten products and specialty metals.

Supply chains showed signs of strain as demand improved. The Supplier Deliveries Index remained at 60.6, its highest level since May 2022, indicating deliveries continued to slow. Slower deliveries typically reflect stronger demand but can also signal supply bottlenecks that complicate inventory planning.

Meanwhile, customer inventories remained unusually lean. The Customers’ Inventories Index registered 42.7, indicating many manufacturers believe their customers’ stock levels remain too low. Historically, low customer inventories have supported future replenishment activity and additional production growth.

Employment remained a weak spot. The manufacturing employment index improved to 48.6 but remained below the growth threshold for the 32nd consecutive month, suggesting companies continue to manage headcounts cautiously despite stronger order activity.

The report points to a manufacturing sector that is gaining momentum but remains challenged by inflation and supply constraints. ISM said the May PMI reading is consistent with annualized U.S. economic growth of approximately 2.2%.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: