Why This Matters to Distributors: Consolidation is accelerating across wholesale distribution as strategic buyers and private equity backed platforms deploy billions of dollars to expand scale, geographic reach, and product breadth. For independent distributors, the pace of investment is raising competitive pressure and narrowing the window to define a long-term growth strategy.

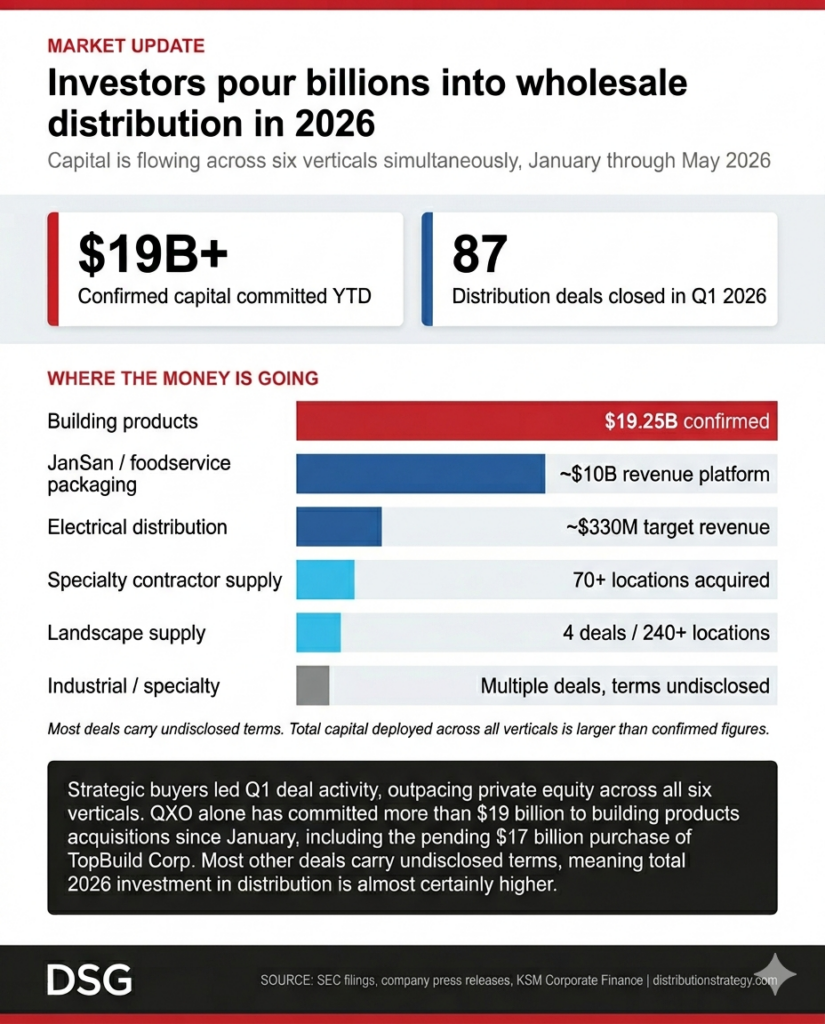

More than $19 billion has been committed to wholesale distribution acquisitions during the first five months of 2026, led by major transactions in building products distribution and a steady stream of deals across electrical, janitorial and sanitation, landscape supply, and specialty industrial markets.

The surge in investment comes as merger and acquisition activity rebounds from a slowdown in late 2025. Distribution deal volume reached 87 transactions in the first quarter, up from 74 in the fourth quarter, according to data compiled by KSM Corporate Finance, which tracks acquisition activity across automotive, building products, food and beverage, healthcare, industrial and technology distribution sectors.

Building products distribution accounted for the largest share of disclosed investment activity, driven entirely by acquisitions announced by QXO.

The company completed its $2.25 billion acquisition of Kodiak Building Partners on April 1 and announced an agreement 18 days later to acquire TopBuild for approximately $17 billion. Together, the two transactions represent more than $19 billion in announced acquisition spending this year.

If completed, the TopBuild transaction would rank among the largest acquisitions in the history of building products distribution. The deal values TopBuild at approximately $505 per share and is expected to close in the third quarter, subject to shareholder and regulatory approval. Based on 2025 results, the combined company would generate more than $18 billion in annual revenue and operate approximately 1,150 locations across the United States and Canada.

Consolidation activity extends well beyond building products.

In March, janitorial and sanitation distributors Imperial Dade and BradyPLUS completed their previously announced merger, creating a company with approximately $10 billion in annual revenue. The combined organization, operating as Imperial Brady, serves customers across the United States and Canada in janitorial supplies, foodservice products, and industrial packaging. Financial terms were not disclosed.

Electrical distribution also remained active. In May, French electrical distributor Rexel agreed to acquire Revere Electric Supply, an Illinois distributor with approximately $330 million in annual sales and a strong position in industrial automation. On the same day, Graybar announced the acquisition of American Electric Supply in California. Financial terms were not disclosed for either transaction.

Private equity investors also continued to target specialty distribution platforms. Leonard Green & Partners acquired NEFCO Holding Co., a distributor of construction fasteners and contractor supplies, while Distribution Solutions Group expanded its presence in Canada through the acquisition of Eastern Valve and Control Specialties, a supplier of industrial valves and instrumentation products.

Landscape supply remained another active area for consolidation. Heritage Landscape Supply Group, a subsidiary of SRS Distribution, completed four acquisitions during the first four months of the year, expanding its footprint in Florida, Nebraska, and Illinois. The company now operates more than 240 locations across 37 states. Financial terms were not disclosed.

The makeup of buyers is shifting as well.

According to KSM, strategic acquirers accounted for the largest share of first quarter transactions, outpacing both private equity firms and hybrid buyers. Corporate acquirers focused on geographic expansion, adjacent product categories, and operating efficiencies, while private equity firms concentrate primarily on acquisitions for existing portfolio companies rather than launching new distribution platforms.

For distributors, the investment surge underscores how quickly competitive dynamics are changing. Large strategic buyers and private equity backed companies continue to acquire local and regional operators, creating larger organizations with broader product portfolios, deeper resources, and wider geographic coverage.

While most transaction values remain undisclosed, the volume of activity suggests capital continues to flow aggressively into distribution. Companies that have not defined their position in the consolidation cycle, whether as acquirers, acquisition targets or independent operators, may find themselves competing against rivals with significantly greater scale and financial backing.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: