Why This Matters to Distributors: Wholesale demand remains healthy and hiring has resumed, but distributors continue to face higher costs and supply constraints for products tied to data centers, electrical infrastructure and industrial construction, keeping inventory and sourcing strategies in focus.

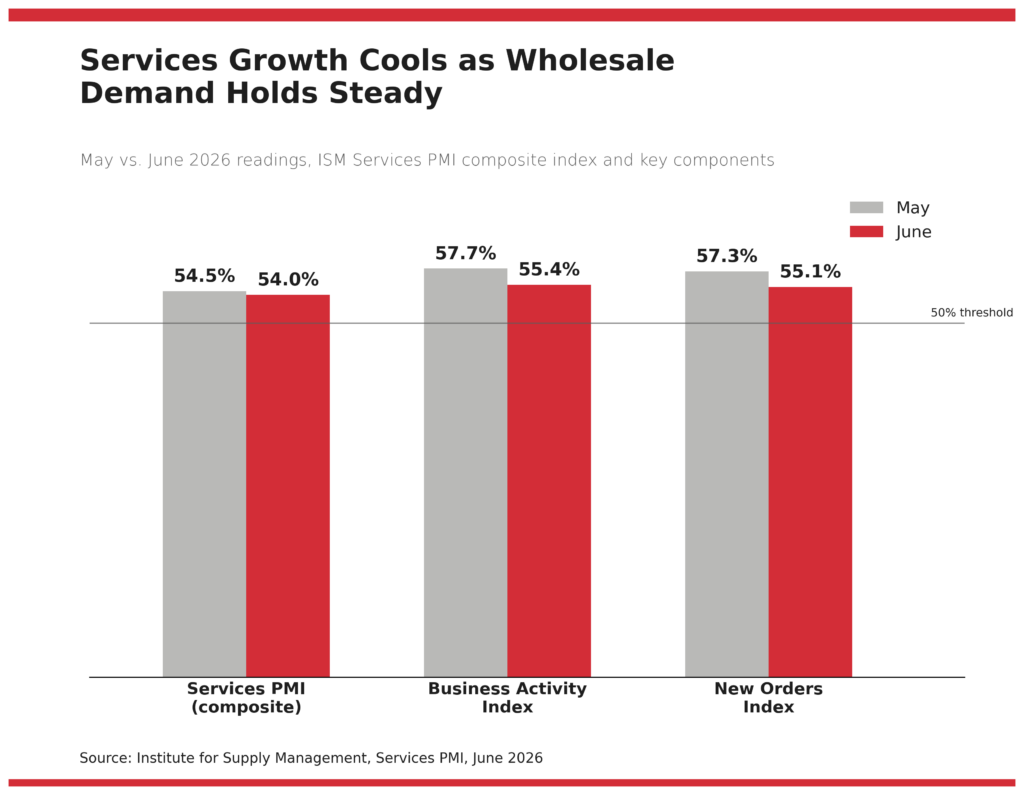

U.S. service-sector activity expanded for the 24th consecutive month in June, although growth moderated as business activity and new orders cooled from May, according to the Institute for Supply Management’s monthly Services Purchasing Managers Index released Monday.

The Services PMI registered 54.0% in June, down from 54.5% in May but remaining above the 50% threshold that signals expansion. The Business Activity Index fell to 55.4% from 57.7%, while the New Orders Index declined to 55.1% from 57.3%. Despite the slower pace, all four components of the composite index remained in expansion territory.

Employment provided a brighter spot. The services employment index returned to growth for the first time in four months, rising to 51.2% from 47.9% in May, signaling that companies resumed modest hiring.

Wholesale trade was among 14 industries reporting growth during June, joining transportation and warehousing, construction, utilities, retail trade and information services. Four industries contracted during the month: agriculture; educational services; management of companies and support services; and public administration.

Supply chain conditions continued to improve, although delivery times remained extended. The Supplier Deliveries Index registered 54.4%, marking the 19th consecutive month of slower deliveries. Because the index is measured inversely, readings above 50% indicate suppliers are taking longer to fulfill orders, typically reflecting stronger demand.

Price pressures eased but remained elevated. The Prices Index fell to 67.7%, its lowest level since February, as fuel prices moderated following a decline in crude oil prices. However, respondents continued to report rising costs for copper, aluminum, electrical components, heating, ventilation and air conditioning equipment, software licenses and labor.

Supply constraints also persisted for products tied to power infrastructure and data center construction. Survey respondents reported shortages of transformers, switchgear, wire and cable, electronic components and memory products as demand from artificial intelligence and data center projects continued to strain supply.

Respondents across several industries cited tariffs, higher material costs and longer lead times as ongoing challenges. Wholesale trade companies reported continued revenue growth driven primarily by higher prices, while procurement teams described increasing complexity in managing tariffs, import costs and supplier capacity.

Inventories returned to more typical levels after several months of stockpiling. The Inventories Index fell to 51.2% from 62.5% in May, suggesting businesses have largely completed earlier efforts to build inventory ahead of anticipated tariffs and supply disruptions. Meanwhile, the Backlog of Orders Index rose to 54.9%, its second-highest reading in nearly four years, indicating demand continues to outpace fulfillment in parts of the services economy.

ISM said the June Services PMI reading is consistent with annualized real gross domestic product growth of approximately 1.9%, extending the overall U.S. economic expansion to 73 consecutive months.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: