Why This Matters to Distributors: A 3.3% annual inflation rate powered by surging energy costs is compressing freight budgets, repricing commodity inventory and forcing distributors in every major vertical to recalibrate their pricing strategies in real time.

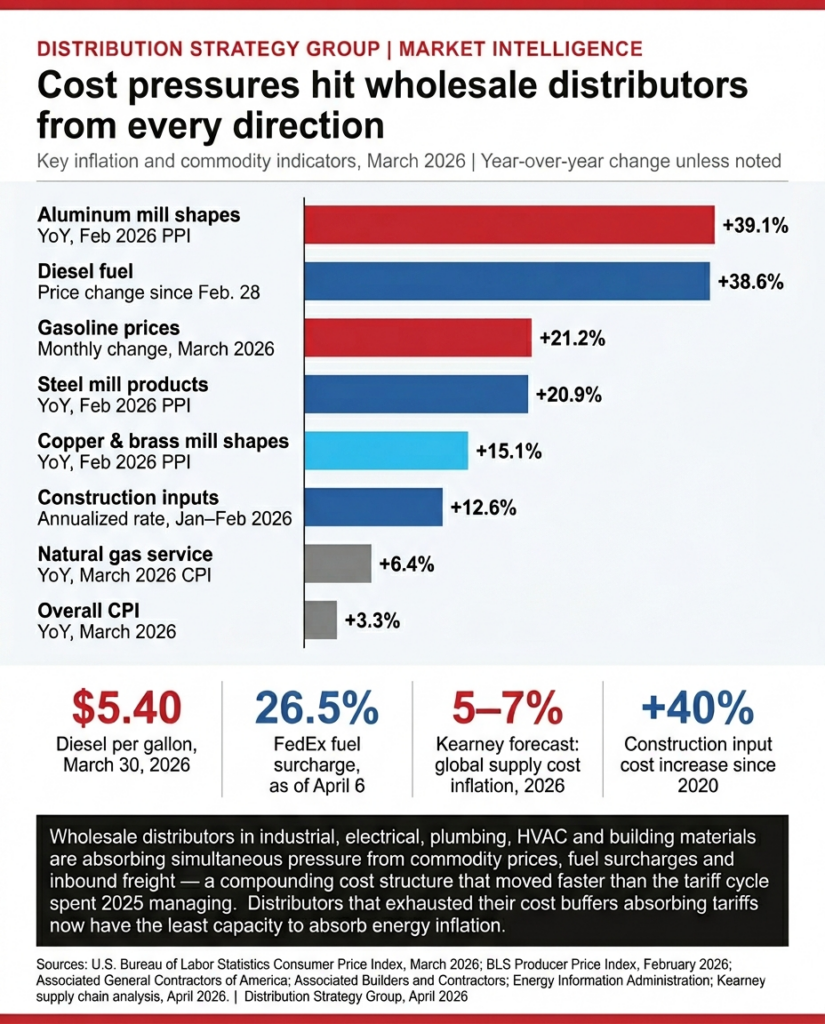

Wholesale distributors are absorbing the sharpest inflation shock in two years, as surging energy prices triggered by the U.S.-Israeli military conflict with Iran drove the Consumer Price Index up 3.3% year-over-year in March — the highest annual rate since May 2024. The Bureau of Labor Statistics reported that consumer prices rose 0.9% monthly, triple the 0.3% pace recorded in February, with a 10.9% spike in energy costs accounting for three-quarters of the monthly increase. Gasoline alone surged 21.2% in March, the largest single-month gain since 1967.

The conflict, which began Feb. 28 with joint U.S.-Israeli strikes on Iran, has severely disrupted traffic through the Strait of Hormuz, a chokepoint that handles 20% of global oil supply and significant volumes of liquefied natural gas. Brent crude climbed from approximately $73 a barrel before the war to near $96 by early April. Even with a ceasefire announced in late March, economists and supply chain analysts say the inflationary effects will continue to ripple through global supply chains for months.

For wholesale distributors, the CPI report documents a cost environment that is structurally more difficult than the tariff cycle they have been managing for the past year — because energy-cost inflation moves through commercial contracts faster and with less ability to hedge or absorb than tariff-driven price increases. Businesses spent much of 2025 absorbing tariff costs without passing them through. With freight and energy expenses now spiking simultaneously, that buffer has been exhausted.

Freight Costs Reprice Across the Board

Transportation is the first and most direct pressure point. Diesel prices rose 38.6% to $5.401 a gallon by March 30, the Energy Information Administration reported, lifting fuel surcharges and spot freight rates across U.S. trucking markets simultaneously.

The repricing has been swift and broad. FedEx raised its fuel surcharge to 26.5% as of April 6. The U.S. Postal Service, which had never previously imposed a fuel surcharge, implemented an 8% surcharge on packages effective April 26, with the fee set to remain through at least January 2027. Amazon announced a 3.5% fuel and logistics surcharge for third-party sellers in the U.S. and Canada taking effect April 17. Ocean carriers, including Maersk, have added separate war-risk and rerouting fees on top of elevated bunker surcharges.

For distributors whose freight contracts were negotiated in the fourth quarter of 2025, those agreements are now fundamentally misaligned with carrier economics. Consulting firm Kearney revised its 2026 forecast for global supply cost inflation to between 5% and 7%, up from a prior estimate of 2.3% to 4%, noting that — unlike tariffs — energy costs pass through to commercial contracts directly and immediately. Contract carriers are expected to move surcharges first, with linehaul rate adjustments following in the second quarter.

Industrial Distribution: Metals and Energy Compression Arrive Together

Industrial distributors are absorbing price pressure from two directions simultaneously. According to Bureau of Labor Statistics producer price index data analyzed by the Associated General Contractors of America, aluminum mill shapes rose 39.1% year-over-year through February, steel mill products climbed 20.9% and copper and brass mill shapes increased 15.1% — all the largest annual gains since the supply-chain disruptions of early 2022. Fabricated structural metal, bar joists and rebar were up 20% over the same period.

Those metals are core inventory for industrial distributors serving manufacturing, heavy equipment, and infrastructure accounts. For MRO distributors particularly, the combination of commodity inflation, sharply higher inbound freight costs, and the exhaustion of pretariff inventory buffers is compressing margins on the highest-volume products in their catalog.

The customers they serve are also pulling back. Associated Builders and Contractors reported that construction input costs rose at a 12.6% annualized rate during the first two months of 2026 — before Iran-war energy costs were factored in. U.S. construction spending declined in January, with private construction spending falling 0.6% and construction payrolls dropping 11,000 jobs in February as contractors delayed new hiring amid pricing uncertainty.

Electrical Distribution: Structural Pressure, Now Amplified

Electrical distributors were already managing sustained commodity cost inflation before the Iran conflict began. BLS producer price index data shows copper wire and cable as well as switchgear costs were up more than 11% year-over-year and roughly 60% from 2020, driven by Section 232 tariffs on aluminum, steel and copper that remain in place and by surging demand from data center construction, grid infrastructure upgrades and electrification projects.

The war has added volatility to copper markets, though the price dynamics are complex. Copper was trading at approximately $13,439 per metric ton on the London Metal Exchange before hostilities began Feb. 28 and has since pulled back to near $12,955 per metric ton — a decline of 3.6% as recession concerns tied to inflation and higher interest rates weigh on demand expectations. That price movement, however, still leaves copper 30% above its 2025 annual average. For electrical distributors with open purchase orders on wire, conduit and switchgear, the volatility complicates cost-plus pricing conversations with customers on projects that were bid before the war began.

Electricity costs for commercial and industrial end customers rose 0.8% in March alone and are up 4.6% over the past year, according to the BLS CPI report — a trend that raises operating costs for the businesses electrical distributors serve while simultaneously driving the grid and efficiency investment that generates demand for the products they stock.

Plumbing and HVAC Distribution: A Second Wave of Manufacturer Increases

Plumbing, heating, cooling, and pipe-valves-fittings distributors entered 2026 already managing a cycle of manufacturer price increases driven by tariffs on Asian imports, which account for a large share of domestic plumbing-related goods. The Iran conflict has layered added cost pressure on top of that existing cycle.

The spring 2026 repricing wave in the plumbing-HVAC-PVF channel has been extensive. According to Supply House Times and Plumbing & Mechanical, the following manufacturer increases took effect between late March and mid-April: Charlotte Pipe, 10% on PVC and CPVC plastic pipe (effective March 26); Honeywell, 5% across its plumbing and HVAC product lines (April 1); IPEX, 10% (April 6); National Comfort Products, 7% (April 16). Merit Brass announced a 6% to 12% increase effective March 23. Those adjustments cover venting systems, brass fittings, PVF components, thermoplastics, and copper-based products — the full width of a plumbing distributor’s stocking catalog.

The underlying commodity picture explains the breadth of the increases. Copper prices have risen 38% over the past year, affecting every plumbing project. Steel used in brackets, hangers, and fittings costs 21% more than a year ago. PVC and CPVC prices have risen sharply on supply shocks and feedstock inflation tied to petrochemical inputs that are directly exposed to energy price volatility.

HVAC distributors face the same commodity-cost dynamics plus a demand-side complication. The year opened with a wave of manufacturer increases — most in the low- to mid-single-digit range, with some reaching double digits — across parts, accessories, filtration, insulation, and commercial equipment. Those January adjustments, documented by The ACHR News, arrived before the Iran war drove energy and refrigerant costs higher. HVAC distributors are now managing a second pricing cycle, on top of one their contractor customers have not yet fully passed through to end users. Natural gas service costs are up 6.4% from a year ago, directly affecting the operating economics of the commercial and residential customers that drive service and replacement volume.

Building Materials Distribution: The Broadest Commodity Exposure

Building materials distributors carry the widest exposure of any distribution vertical to the current inflation environment, with inventory spanning every category under the most severe cost pressure: steel, aluminum, copper, lumber, PVC, and concrete inputs.

Construction input costs have risen more than 40% since early 2020, and the Associated Builders and Contractors reported a further 3.7% year-over-year increase in nonresidential construction input prices through February. The CRU Global Flat Products Price Indicator stood at 210.9 in April, up 3% month-over-month, with the Middle East conflict identified as the principal factor driving steel price increases as energy costs ripple through steelmaking and transportation simultaneously.

Aluminum presents a particularly acute supply risk for building materials distributors stocking structural and fenestration products. Military strikes on aluminum facilities in the United Arab Emirates and Bahrain have disrupted a Gulf Cooperation Council market that Wood Mackenzie analysts had already forecast would run a 200,000-metric-ton global deficit in 2026, widening to 800,000 metric tons by 2028. There are no viable short-term alternatives to offset production losses in the region.

The demand environment has deteriorated at precisely the wrong time. Thirty-year mortgage rates climbed back to 6.5% in the first week of April, according to Steel Market Update, suppressing residential construction starts and the downstream order flow that building materials distributors depend on for volume. The construction sector pulling back on project starts while input costs are rising is the most difficult environment for a building materials distributor to manage pricing and inventory simultaneously.

The Forward Inflation Risk Is Not Contained

The March CPI data does not mark the peak of this inflationary cycle. Economists cited by Kiplinger estimate that even if the Iran conflict ends and gasoline prices return to pre-war levels, core inflation — which excludes food and energy — is likely to approach 3% by year-end, pushed by continued tariff effects and rising service costs. The energy lag is a significant factor: historical data show that energy price spikes typically take three to six months to fully filter through to goods prices, meaning the full cost impact of March’s energy shock has not yet appeared in most supplier invoices.

The Federal Reserve held the federal funds rate at 3.5% to 3.75% at its March meeting and indicated one rate cut for 2026, according to the BLS and Federal Reserve meeting records — a posture that keeps borrowing costs elevated for distributors financing inventory or capital expenditures for most of the year. The Fed’s next scheduled policy meeting is April 28-29.

The operating environment for wholesale distributors through mid-2026 is defined by a cost structure that is being pressured from multiple directions without a single lever to relieve it. Electrical, plumbing, HVAC and building materials distributors face commodity input costs tied directly to the metals, resins, and energy feedstocks under the sharpest pressure. Industrial distributors face those same input cost dynamics against a backdrop of slowing customer demand. The distributors best equipped to protect margins are those that have built dynamic pricing systems, diversified their carrier networks, and converted freight agreements to floating-fuel structures. Those still absorbing costs on fixed contracts will find the second quarter a significantly harder test than the first.

Share this article: