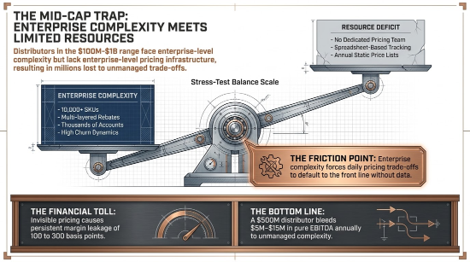

If you run a distribution business between $100 million and $1 billion in revenue, you know the feeling. You carry the complexity of a large enterprise — thousands of accounts, tens of thousands of SKUs, multiple warehouses, layered rebate programs, regional competitors who price differently in every market — without the enterprise’s pricing team, its data scientists, or its appetite for a seven-figure software bill. You’re caught in the middle.

That middle is an expensive place to sit. Most mid-cap distributors leak 100 to 300 basis points of margin a year, quietly and continuously. For a $500 million distributor that’s $5 million to $15 million in profit walking out the door annually, usually with no one accountable for getting it back. Leadership teams sense the problem; what they rarely have is a path to fix it that doesn’t mean overbuying technology or blowing up the commercial organization.

This article lays out that path: why mid-caps get stuck, why the obvious fixes disappoint, and what a focused 90-day effort can recover with the people and data you already have. One idea that sits underneath it all — pricing is a market-facing capability, not an internal clean-up project. The distributors who win build the foundation before they buy the tools.

The Trap Nobody Designed

Ask most distributors what’s wrong with their pricing and you’ll hear “too much complexity.” True, but incomplete. The real problem is that complexity forces trade-offs — margin versus volume, retention versus expansion, this account versus that one — and in most mid-cap firms those trade-offs happen by default, deal by deal, rep by rep, with no shared logic, no common data, and no accountability. The result isn’t bad pricing so much as invisible pricing. You can’t manage what you can’t see.

You’ve been told pricing is the most powerful lever on the P&L. That’s correct, and routinely misunderstood. Improving price doesn’t always mean raising it — sometimes the right move is to hold flat or cut to protect a key account or defend share. But without visibility into how customers behave and where you have pricing power, every action is a blunt instrument: some create value, some destroy it, and you can’t tell which until the annual review lands. A Revify Analytics survey of more than 250 commercial leaders found only about one in ten mid-market companies consistently uses analytics to drive pricing, and 77% sit at low or medium maturity in turning insight into frontline execution.

This is a uniquely mid-cap problem. A small distributor runs on the owner’s instinct and a sharp CFO; a large one hires a pricing department and buys the platform. The firm in the $200 million to $800 million range gets enterprise complexity on a constrained budget — too complex for instinct, too lean for the enterprise playbook.

What Stuck Looks Like

The symptoms are familiar: pricing run out of spreadsheets, similar accounts getting wildly different discounts, nobody sure what the margin is after deductions. Those are surface signs. Underneath are a handful of specific gaps — each pointing to a takeaway you can act on.

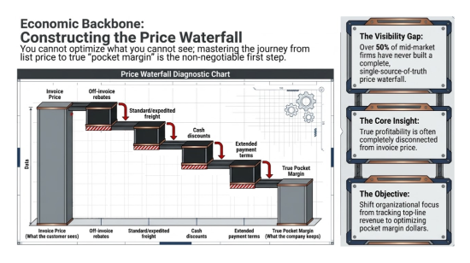

You can’t see the price waterfall. Most distributors know the invoice price; far fewer can see pocket margin — what’s left after rebates, discounts, freight, payment terms, and special pricing agreements. More than half the mid-market firms Revify has diagnosed had never built a complete waterfall connecting list price to pocket margin. That’s not a technical gap; it’s a strategic blind spot. Build the waterfall first.

Reps price without guardrails. When reps set price on gut, history, and customer pushback, you get inconsistency across the same segment — and a bias toward conceding, because reps answer for lost deals far more than for underpricing. Publish floors and approval authority.

Discounts vary for no good reason. Plot discount depth against customer size and two patterns jump out: small customers getting deep discounts, and strategic accounts getting worse terms than they should. Outliers also cluster around reps or product lines — each is recoverable margin hiding in plain sight.

Rebate programs have gone stale. Many haven’t been touched in years — rewarding volume thresholds that no longer make sense and paying customers who no longer qualify, while ignoring growth, mix, and profitability. Few mid-caps run a rigorous annual rebate audit, and the self-inflicted loss adds up fast.

Nobody owns pricing. Sales, finance, category, and operations all touch price; no one is accountable for realizing it. Left ownerless, it drifts toward lower prices and deeper discounts. Name an owner.

The price list is frozen in a moving world. Most mid-caps still run annual price lists while supplier costs move monthly, tariffs shift quarterly, and competitors reprice weekly. Revify research puts the cost of that lag at 8 to 11% of recoverable profit. The fix isn’t real-time dynamic pricing — it’s reviewing your biggest revenue segments monthly or quarterly instead of once a year.

Why Buying Software Won’t Save You

When the problem finally gets attention, leadership often reaches for a pricing system — a logical instinct and a frequent disappointment.

Automating a broken process produces broken decisions faster. If your pocket-margin view is wrong because rebates sit off-invoice and freight lives in another system, any algorithm you layer on will optimize the wrong target. AI on bad data is fast, precise, and wrong. In Revify’s 2025 maturity research, only about 10% of mid-market firms ranked high on the foundational capabilities any pricing engine needs as inputs — data governance, waterfall visibility, discount discipline. The tools are ready; the data underneath usually isn’t.

No tool fixes cross-functional misalignment, either. Sales wants volume, finance wants EBITDA, operations wants capacity. Until leadership aligns those objectives and the governance behind them, a pricing tool just generates recommendations people override. Adoption collapses without a foundation: industry estimates show fewer than one in five major analytics and AI transformations deliver the value expected. For a mid-cap, a stalled platform isn’t just wasted capital — it sets pricing back two or three years.

The distributors who deploy technology successfully almost never start with the tool. They start with strategy, set governance and decision rights, stabilize the data, capture the quick wins that fund the rest, and only then automate to scale what works. Diagnose, stabilize, optimize, scale — in that order. Even a one-point margin gain can return five to ten times the investment. Technology amplifies a working pricing function; it amplifies the problems in a broken one just as efficiently.

What to Put in Place First

None of the groundwork requires a big budget — just executive commitment and a few people willing to work across functions.

Start with a unified, transaction-level view of profitability — discounts, rebates, freight, payment terms, and costs pulled from ERP, finance, and program spreadsheets into one format.

From there, add a grounded read on demand and competition — willingness to pay inferred from past price responses, competitive position from lost-deal reviews and periodic price checks. Define a short set of KPIs with named owners: price realization versus target, pocket margin by segment, discount distribution, override rate, and quote cycle time.

Govern it through a Pricing Council, not a department — a cross-functional group led by a senior executive, meeting on a fixed cadence with published floors, tiered discount authority, and a clear approval workflow. Then align incentives, the step most firms skip. If reps are paid on revenue or gross-margin percent rather than gross-profit dollars, discipline won’t stick; shifting even 10 to 20% of variable pay toward profit dollars changes behavior. In one Revify engagement, a retailer paid advisors on margin percent, which quietly undercut total profit — the incentive had to be fixed before the analytics could take hold. Finally, enable the people who price in front of the customer: train them, give them materials they can defend, and certify your best performers as coaches. Sharpen human judgment, don’t replace it.

90 Day, No Seven-Figure Check

Ninety days is long enough to make real progress and short enough to build momentum. Here’s how to spend it with the resources you have.

Days 1–30: see it. In week one, name a single accountable owner — CFO, COO, or a senior commercial leader — and stand up the Pricing Council. That step costs nothing and matters most. In parallel, pull twelve months of transactions, add rebates and allowances, reconcile freight and payment terms, and build the waterfall — a credible pocket-margin view by week three, imperfect is fine. Then run a discount-variability analysis: for each major product family, plot discount depth against deal size, customer size, and strategic tier, and flag the outliers. Clean analysis like this typically surfaces one to three points of recoverable leakage. Close the month with a one-page baseline scorecard as the Council’s standing first agenda item.

Days 31–60: act on it. Assign the 50 to 100 highest-leakage customer-product combinations to named owners with a specific plan — renegotiate, reprice, or phase out — and a 60-day deadline. This is the hard part and usually the biggest first-year payoff. Publish a price-floor and approval-authority matrix by product family and enforce it in existing systems. Audit every rebate and vendor program; kill what’s outdated and modernize at least one toward growth or profitable mix rather than raw volume. Stand up basic segmentation too: sort accounts into three or four tiers, then check whether your best customers get your best prices. They often don’t — and fixing it helps margin and the relationship at once.

Days 61–90: make it stick. Without reinforcement, organizations snap back. Work with HR and finance to make at least one real change to the comp plan — more weight on gross-profit dollars, a margin-discipline component, or a cap on variable pay for below-floor deals — and pilot it in one region next quarter. Run a half-day sales training on real pipeline deals using the new floors and workflow. And shift the cadence: commit to monthly or quarterly list-price reviews for at least the top 20% of SKUs by revenue. A pragmatic, rules-based approach gets most of the value with none of the heavy investment.

Notice what’s not on the list: no pricing software, no new pricing function, no data-science hires. Those belong in a later phase once the foundation is built and early wins have paid for them. Expect resistance — from reps used to flexibility, customers losing structural discounts, and stakeholders attached to the status quo. The firms that treat pushback as a normal part of change, not a reason to slow down, get through.

What You’ll Do at Day 90

Four things: a working pricing council with an executive owner and a scorecard it actually revisits; a defensible pocket-margin view the CFO, sales, and CEO all trust as the single source of truth; early margin recovery from outlier remediation — typically 30 to 70 basis points in the first two quarters, with more compounding behind it; and a twelve-month roadmap the leadership team has aligned on.

Not all leakage is recoverable, and some volume loss comes with the territory. A few relationships may end, and a few reps may leave over the new discipline. Successful organizations treat those as costs of the transformation, not reasons to reverse it.

The biggest change is cultural. Pricing moves from a reactive chore to a strategic discipline run with the same rigor as cost or working capital — and once that shift happens, capturing incremental gains every year gets easier. The magnitude is real: across distributor quick-win engagements, 5 to 20% gross-profit improvements are typical.

The Bottom Line

Pricing stays broken in mid-cap distribution not because the problems are unsolvable, but because they span functions, force hard trade-offs, and lack a natural owner. Technology helps — but only after the fundamentals are in place. Sequencing is what separates the distributors that break out from those that cycle through initiatives for years without landing one.

Focus on what endures: people, process, and a culture of deciding from insight. Let the tools amplify that foundation, not substitute for it — build a capability, not a crutch. You don’t need to match enterprise sophistication to earn enterprise-grade returns. You need to stop running pricing out of spreadsheets and start treating it as the highest-ROI lever on your P&L.

Share this article: