Why This Matters to Distributors: Ferguson is accelerating its shift toward higher-margin, technical distribution businesses serving industrial growth markets. The acquisition strengthens its capabilities in valve automation and flow control while increasing competitive pressure on regional distributors serving data centers, semiconductor plants, power generation and other process industries.

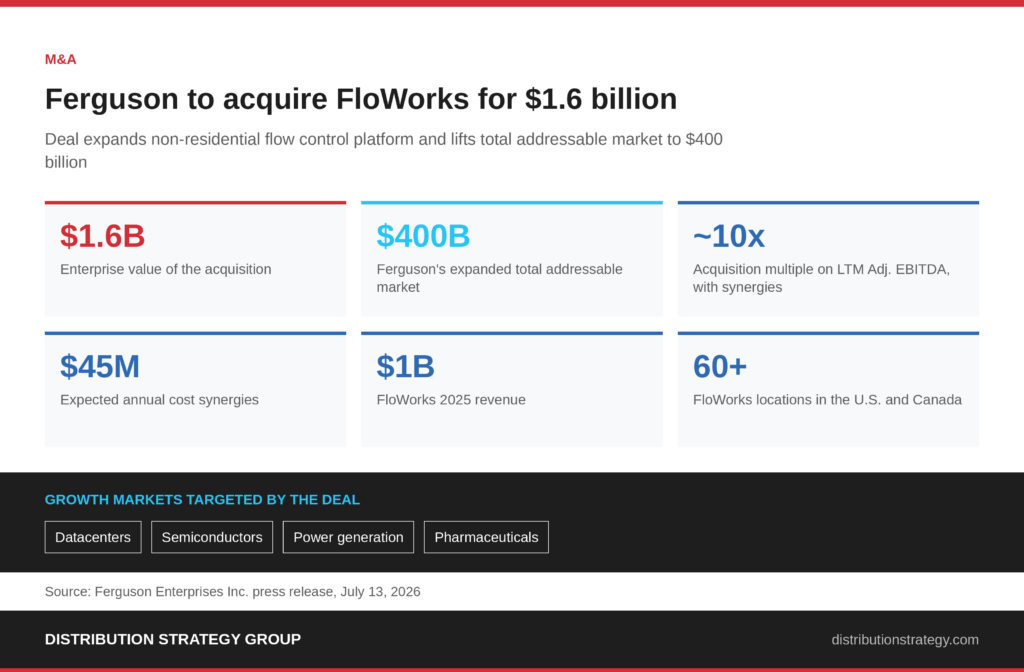

Ferguson Enterprises Inc. has agreed to acquire Houston-based FloWorks from private equity firm Wynnchurch Capital for approximately $1.6 billion in cash, expanding its industrial distribution business and deepening its presence in technical flow control markets.

The transaction, announced Monday, is expected to close in the third quarter, subject to customary regulatory approvals and closing conditions.

FloWorks distributes and services engineered valves, valve automation systems and related flow control products used in chemical processing, refining, power generation, semiconductor manufacturing, pharmaceuticals, and data centers. The company generated approximately $1 billion in revenue in 2025 and operates more than 60 locations across the United States and Canada, including 25 service and repair centers. FloWorks employs more than 1,000 associates and represents a portfolio of 15 industrial brands.

The acquisition expands Ferguson’s industrial platform by adding specialized technical expertise, service capabilities and a stronger presence across the Gulf Coast and southern United States.

“FloWorks strengthens our leading position in high-growth industrial end markets while adding meaningful capabilities and geographic coverage that we can leverage across our nonresidential customer groups,” Ferguson CEO Kevin Murphy said.

FloWorks CEO Scott Jackson said the combination will provide the company with additional resources to expand its technical capabilities and customer service.

Ferguson said the purchase price represents approximately 10 times FloWorks’ last 12 months of adjusted EBITDA, including an estimated $45 million in expected synergies from network optimization, logistics and technology integration. The company expects the acquisition to be immediately accretive to adjusted earnings per share before one-time transaction and integration costs.

The acquisition increases Ferguson’s exposure to maintenance, repair, and operations markets, where recurring service and replacement demand typically produces more consistent revenue than project-driven construction activity.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: