Why This Matters to Distributors: The Federal Reserve’s April Beige Book is the most comprehensive real-time snapshot of business conditions across the U.S. economy. Its findings — costs rising faster than prices, declining wholesale activity, and the most cautious business outlook of 2026 — describe conditions hitting distributors directly.

The Federal Reserve released its April Beige Book on April 16, documenting an economy growing slowly in most regions but deteriorating sharply in terms of business confidence and margin performance, as the conflict in the Middle East added a new energy cost shock on top of the tariff-driven cost pressure that has been squeezing wholesale distributors since 2025.

Overall economic activity increased at a slight to modest pace in eight of the 12 Federal Reserve Districts, while two Districts reported little change and two Districts reported slight to modest declines. The conflict in the Middle East was cited as a major source of uncertainty about the complicated decision-making around hiring, pricing, and capital investment, with many firms adopting a wait-and-see posture. Business outlooks varied amid widespread uncertainty about future conditions.

That final sentence is the sharpest signal in the report. As recently as March, the Fed characterized most businesses as expecting slight to moderate growth. That optimism has given way to what the April Beige Book describes as widespread uncertainty — the most cautious framing in any of the three reports issued so far in 2026.

Wholesale Activity Is Declining

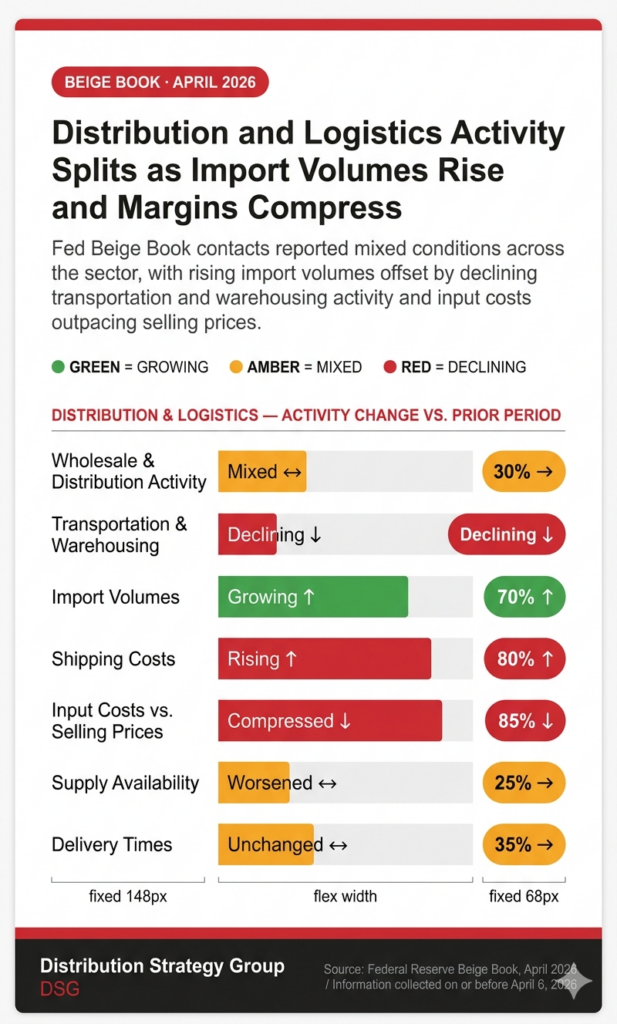

The April Beige Book delivers a specific and unflattering data point: activity declined among wholesale distribution firms the Federal Reserve surveyed. The St. Louis Fed added the granular detail. A wholesale distributor in Illinois reported that economic uncertainty and expectations of future rate changes were delaying new commercial construction starts, reducing bulk orders for materials. A firm in St. Louis reported sales were down about 5% year to date, attributing it to inflation eroding customer purchasing power, leading buyers to defer replacing older non-essential goods and demanding more aggressive pricing.

The New York district offered a similar picture from the manufacturing customer side. Contacts noted greater uncertainty due to changing tariffs and the Middle East conflict, upending pricing schedules and making customers hesitant to commit to purchases. When customers will not commit to purchases, distributors cannot plan inventory, manage lead times, or protect margins. The hesitation runs in both directions through the supply chain.

The defining pressure in the April Beige Book for wholesale distributors is not demand — it is what happened to the relationship between what companies pay for inputs and what they can charge. Price growth mostly remained moderate overall, but input cost increases outpaced selling price growth, compressing margins.

The Cost-Price Gap

The Middle East conflict accelerated this dynamic. Energy and fuel costs rose sharply in all Districts, attributed to the conflict, leading to higher freight and shipping costs and higher prices for plastics, fertilizers, and other petroleum-based products. That finding spans all 12 districts — it is not regional. Every distributor moving goods by truck, rail or ocean container is paying more to do so than in February, and those increases have moved quickly through carrier fuel surcharges and contract rate revisions.

Tariffs are still active on top of the energy shock. Input cost pressures beyond energy-related increases were also widespread. Several Districts reported rising prices for metals due to tariffs, such as steel, copper, and aluminum. Technology costs rose for both hardware and software. Insurance premiums and health care costs continued to climb.

The result is a cost structure that widened materially between March and April. The March Beige Book described firms as selectively passing through tariff cost increases, with some absorbing them and others beginning to pass them through. The April report describes something structurally different: broad margin compression as input costs outrun selling prices across most districts. The Fed’s own characterization of the shift is pointed. “Most firms did not plan to raise prices in the near term, but contacts noted that the pricing outlook was hazy owing to recent cost shocks and lingering uncertainty related to tariffs,” the report stated.

What Customers Are Doing

The demand picture offers little near-term relief. Consumer spending increased slightly overall, but the composition of that growth matters for distributors. Many Districts continued to report signs of consumer financial strain, increased price sensitivity and rising demand at food banks and other social service organizations, while spending among higher-income consumers was resilient.

The residential construction market — a core demand driver for electrical, plumbing, HVAC and building products distributors — softened further. Housing market activity softened across several Districts as heightened uncertainty and rising mortgage rates dampened buyer demand. That is a deterioration from March, when housing was described as declining slightly. Mortgage rate pressure has been added to affordability constraints as a headwind, narrowing the near-term demand outlook for distributors serving residential end markets.

Manufacturing customers, the core account base for industrial and MRO distributors, showed mixed results. Manufacturing activity rose slightly to moderately in most Districts. Data center demand remained a driver, and the Middle East conflict produced some defense-related order increases, though many manufacturers worried that a prolonged conflict would raise input costs and soften demand. Data center and defense demand creates activity in specific electrical, mechanical and specialty categories. It does not lift the broader industrial distribution market, where flat to cautious conditions are the prevailing findings.

Hiring and Investment Are Frozen

The labor market findings in the April Beige Book reflect the same posture distributors are taking across their own operations. Most Districts described labor demand as stable, with low turnover, minimal layoffs and hiring mostly for replacement. Several Districts noted increased demand for temporary or contract workers, as firms remained cautious about committing to permanent hires. While most Districts indicated that AI had not significantly impacted overall staffing levels, some noted that AI-driven productivity improvements had enabled many firms to delay or reduce hiring.

The surge in demand for temporary workers is a direct indicator of how broadly that caution has spread. Contract labor is the hedge companies reach for when they need to fill a role but will not commit to a permanent hire. That pattern is now the national norm across industry sectors. Capital spending is in the same holding pattern. Capital expenditures have paused and are expected to remain subdued due to uncertainty, with one manufacturer noting that expansion designs were progressing, but execution was unlikely for the next 12 months due to market softness.

The April Beige Book does not describe an economy in recession. Eight of 12 districts reported growth. But the direction of change from March to April is unambiguous. The cost structure for distributors has widened. Customer commitment weakened. Wholesale activity declined. Business confidence fell to its lowest point of the year. And both primary drivers of that deterioration — energy costs tied to the Middle East conflict and tariffs on metals and industrial inputs — have no clear near-term resolution.

The March expectation of slower price growth did not materialize. Instead, the cost structure widened, with energy now the dominant price theme layered on top of tariffs that remain fully in effect. For wholesale distributors already operating on thin margins, the combination of rising costs, cautious customers and deferred purchasing decisions makes the second half of 2026 a difficult operating environment to plan for with confidence.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: