Why This Matters to Distributors: QXO’s assembly of a multi-vertical, 1,150-branch platform in under 12 months signals that building products distribution is entering a consolidation phase where scale across product categories — not depth in one — increasingly defines who sets the terms with both manufacturers and customers.

QXO Inc. has agreed to acquire TopBuild Corp., the largest distributor and installer of insulation in North America, for approximately $17 billion. The transaction, unanimously approved by both companies’ boards of directors, is expected to close in the third quarter of and would establish QXO as the second largest publicly traded building products distributor in North America.

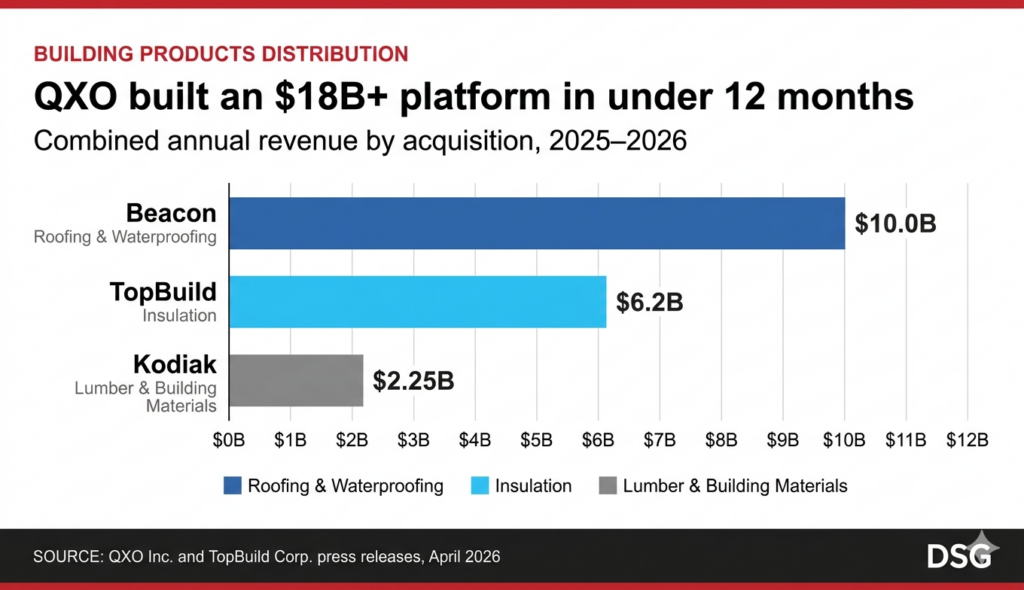

The deal is the third major acquisition QXO chairman and CEO Brad Jacobs has completed in less than 12 months. After closing on Beacon Roofing Supply in 2025 and Kodiak Building Partners on April 1, the addition of TopBuild would bring QXO’s combined company revenue above $18 billion and combined adjusted EBITDA above $2 billion. A year ago, QXO had no building products revenue at all.

The transaction values each TopBuild share at $505, a 23.1% premium to the company’s closing price on April 17. Stockholders can elect cash or QXO stock per share, with the total consideration structured as approximately 45% cash and 55% QXO stock. The deal includes a $600 million breakup fee payable to QXO if the transaction is terminated.

TopBuild is not a simple distributor. It is a vertically integrated platform that both distributes and installs insulation products across residential, commercial, and industrial construction markets — a business model that makes it structurally different from most distributors in the building products supply chain.

What TopBuild Actually Is

The company operates through two primary business segments: TruTeam, a nationwide installation business, and Service Partners, the leading distributor of residential and commercial building insulation products and related accessories in the U.S.

Those two segments are reinforced by a deeper industrial layer. Distribution International and Specialty Products and Insulation are the leading distributors and fabricators of mechanical insulation and related supplies for maintenance, repair, and operations in North America, with products used for thermal, acoustic and firestopping applications across commercial and industrial end markets.

That MRO component matters. Approximately 55% of SPI’s revenue is driven by recurring maintenance and repair, giving TopBuild meaningful exposure to non-cyclical revenue streams, a significant counterweight to the new construction volatility that defines most building products distributors. Approximately 87% of SPI’s revenue is related to commercial and industrial end markets.

TopBuild has completed more than 45 acquisitions since it was spun off from Masco Corp. in 2015, building its distribution and installation footprint through disciplined roll-up strategy. The company provides insulation and commercial roofing installation services nationwide through its Installation segment, which has over 200 branches, and distributes building and mechanical insulation, insulation accessories, and other building products through its Specialty Distribution business.

By the time QXO announced its offer, TopBuild’s Specialty Distribution network encompassed more than 250 branches across the United States and Canada.

Robert Buck, chief executive officer of TopBuild, pointed to the company’s 10-year sales compound annual growth rate of 13% and adjusted earnings per share CAGR of 31% as evidence of the platform’s operational track record. “Together, we’ll enhance customer service, unlock meaningful cross-selling opportunities, and drive continued growth and operating efficiency,” Buck said.

The TopBuild acquisition fills a vertical that QXO did not have. After closing Beacon — a roofing and waterproofing distributor — and Kodiak — a lumber and building materials distributor — QXO had significant scale in above-grade and structural building products but no presence in insulation, a product category present in every construction project.

The combined platform would give QXO No. 1 positions in insulation and waterproofing, No. 2 in roofing, and No. 1 or No. 2 in lumber and building materials in key geographies. QXO’s total addressable market would expand to more than $300 billion.

Jacobs said the deal also expands QXO’s footprint in large, complex construction projects — specifically data centers — where scale and multi-product capability matter. Data center construction has surged across North America in response to AI infrastructure investment, and those projects require significant quantities of insulation, roofing and building materials delivered on aggressive timelines by suppliers capable of handling the scope.

The Strategic Logic for QXO

“The TopBuild transaction will also give us critical mass in the insulation sector and expand our exposure to large, complex projects like data centers, where scale matters,” Jacobs said.

Upon closing, the combined company would have approximately 28,000 employees, more than 10,000 vehicles and 1,150 locations across all 50 U.S. states and seven Canadian provinces. QXO expects approximately $300 million in synergies from cross-selling Beacon and Kodiak products alongside TopBuild’s services, combined with procurement and logistics efficiencies, by 2030. Jacobs said QXO plans to adopt TopBuild’s “special OPS” operational improvement teams across the broader platform, citing TopBuild’s adjusted EBITDA margin of approximately 18% as a benchmark for the combined business.

The TopBuild acquisition accelerates a dynamic consolidation that has been reshaping the building products supply chain for several years, and the implications extend well beyond insulation.

What QXO is assembling is a multi-vertical platform with the procurement scale to pressure manufacturer pricing, the branch density to offer same-day or next-day delivery across most major markets, and the product breadth to serve as a single source for contractors and builders who would otherwise coordinate across multiple distributors.

That combination creates leverage at both ends of the supply chain — with manufacturers, who face a buyer controlling significant volume across multiple product categories, and with customers, who face a supplier capable of bundling products, simplifying procurement, and offering pricing that narrower distributors cannot match.

For regional and single-vertical distributors, particularly those operating in markets where QXO has high branch concentration, the competitive pressure is not theoretical. The building products distribution market is highly fragmented and competitive, with barriers to entry for local competitors relatively low, but that fragmentation cuts both ways. It gives consolidators like QXO a long runway of acquisition targets, and it means the distributors competing against a 1,150-location platform with $18 billion in revenue are doing so without equivalent scale in procurement, technology, or logistics.

TopBuild’s industrial MRO business adds a dimension that is particularly relevant for industrial distributors. Distribution International and SPI compete directly in markets served by large industrial distributors — thermal insulation, acoustic insulation and firestopping products for plants, refineries, and commercial facilities. With those businesses now folded into a QXO platform that also controls roofing and lumber supply, industrial distributors that have treated insulation as a separate competitive lane may find that lane narrowing.

The transaction is designed to strengthen the free cash flow generation necessary to fund continued acquisitions. QXO’s long-range targets — $50 billion in annual revenue and $7.5 billion in adjusted EBITDA — depend on sustaining the same pace that produced the Beacon, Kodiak and TopBuild deals in less than a year. Whether Jacobs can integrate three major platforms simultaneously while maintaining service levels and executing synergies will be the test that determines how quickly that competitive distance grows.

Share this article: