Why This Matters to Distributors: Fastenal is combining AI-enabled sales tools with a more acquisitive international strategy to accelerate growth and deepen large-account relationships. Regional distributors relying on organic expansion and manual quoting face greater pressure as larger competitors shorten sales cycles and expand global capabilities.

Fastenal Co. used Dan Florness’ final earnings call as chief executive officer to signal that its leadership transition will not bring a strategic reset.

Instead, the industrial distributor plans to accelerate the strategy behind its recent market share gains, with artificial intelligence, managed inventory technology and potential acquisitions playing larger roles in its next phase of growth.

Jeff Watts, Fastenal’s president and chief sales officer, succeeds Florness as CEO on July 16. Florness has led the company since 2016 and joined Fastenal in June 1996.

“This isn’t a transition,” Watts said during Fastenal’s July 15 second-quarter earnings call. “We’re sticking with the strategy that we’ve dealt with for the last two years.”

Watts said Fastenal will continue pursuing three priorities: increasing sales effectiveness, enhancing service capabilities, and expanding its addressable market.

The strategy continued to produce strong financial results in the second quarter.

Fastenal reported net sales of $2.39 billion for the quarter ended June 30, up 15.2% from $2.08 billion a year earlier. Net income increased 15.9% to $382.8 million, or 33 cents per diluted share, compared with $330.3 million, or 29 cents per share, in the second quarter of 2025.

Operating income rose 15.1% to $501.8 million, while operating margin remained unchanged at 21%.

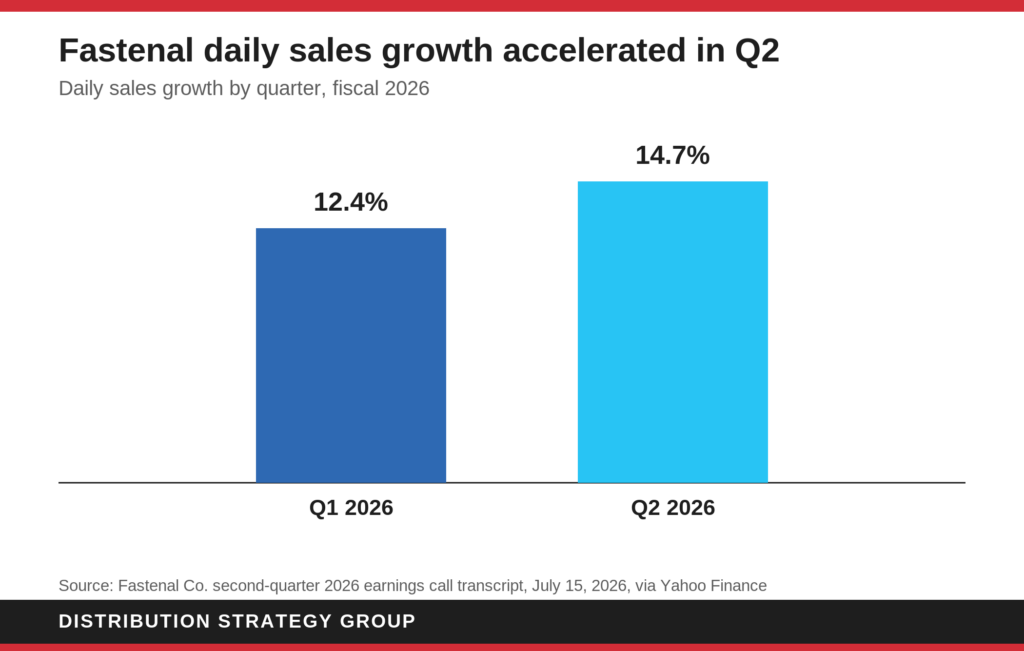

Average daily sales increased 14.7% during the quarter, up from 12.4% in the first quarter. Executives attributed the improvement primarily to market share gains rather than a broad acceleration in industrial demand.

“Our outperformance continues to be driven by share gains and not by the market backdrop,” Watts said.

Contract count increased more than 7% from a year earlier, while the number of customer locations spending at least $50,000 per month climbed 16.5%. Revenue from those larger customer sites rose more than 26%.

“That’s the shape of durable, high-quality revenue: larger customers, deeper contracts and higher productivity per site,” Watts said. “It’s exactly what our key account strategy is designed to produce.”

Technology remains central to Fastenal’s strategy.

Fastenal Managed Inventory, or FMI, represented 44.6% of total sales during the quarter. The company signed an average of 109 weighted FMI devices per day, up 8.3% from a year earlier.

Fastenal’s Digital Footprint, which includes electronically enabled transactions and certain FMI-related sales, represented 61.6% of total sales. That was up 60 basis points from a year earlier.

Watts described each new device installation as a long-term investment in customer retention, sales growth, and operating efficiency.

“Devices installed today are deposits into next quarter’s sales, into next year’s retention and into the operational rigor and efficiency that show up in our margin structure,” he said.

The call also signaled that Fastenal may become more willing to use acquisitions to accelerate international expansion.

Fastenal built its Canadian and Mexican operations organically, using the U.S. supply chain to support their early development. Watts said acquisitions could shorten the time required to establish supply chain infrastructure in other countries.

“When we look at international, when we talk about M&A or acquisitions in the future, trying to take that timeframe from we could build it in 10 years, we could buy it and have that supply chain built in two to three, four maybe, is really a focus for us moving forward,” Watts said after discussing a recent visit to Fastenal’s Italian operations.

The comments did not amount to an announced acquisition program or transaction. However, they indicated that Fastenal is increasingly willing to consider buying infrastructure rather than relying exclusively on organic development in new international markets.

Florness said Fastenal’s standardized technology platform gives the company an advantage with multinational manufacturers seeking consistent inventory and supply chain systems across facilities.

“If you have a manufacturing facility in Chicago, you have one in Romania, Italy, China, we have the same tools, the same solutions in all of the countries that we’re in today, all on the same platform,” Florness said. “Our customers want it, and they want it fast.”

Artificial intelligence was another major theme during the call.

Executives said internally developed AI and quoting tools are helping Fastenal implement newly signed large-account business more quickly.

“A lot of the business that we’re turning on, we’re turning it on faster now because of the tools that we’ve built,” Watts said.

Watts said one-time orders contributed to June sales growth of approximately 20% from a year earlier, a result that exceeded management’s expectations. Florness later said June growth was “north of 20%.”

Florness said AI tools are improving productivity by accelerating quoting and allowing Fastenal to activate large-account business faster than it could in previous years.

“We’re implementing large account business faster today than we would have one, two and three years ago because we can do quotes faster,” Florness said.

“A lot of companies are talking about AI,” he added. “We don’t talk a lot about it. We just do a bunch of things behind the scenes to have better tools to support our people and our customers.”

Florness said Fastenal spends approximately $1.6 billion annually on employee-related costs and evaluates AI investments partly by whether they can make that workforce 5% to 10% more productive.

The company’s growth was broad based across its industrial markets.

Heavy manufacturing, which represented 44% of total sales, grew approximately 18% during the quarter. Construction sales increased about 17% for a second consecutive quarter, supported by electrical, utility, infrastructure, and data center activity.

Executives also cited growth in transportation, warehousing, and other industrial services.

Gross margin declined approximately 75 basis points from a year earlier, including a 40-basis-point headwind from the relationship between pricing and product costs. Customer mix, transportation costs, and rebates also weighed on gross margin.

Chief financial officer Max Tunnicliff said the shift toward larger strategic accounts is intentional. Those customers typically carry lower gross-margin percentages but generate greater profit dollars and operating efficiencies through higher volumes, improved asset utilization, and fixed-cost leverage.

Selling, general and administrative expenses declined to 23.5% of sales from 24.4% a year earlier. That operating leverage helped Fastenal maintain its operating margin despite gross-margin pressure and continued investments in technology, analytics, and sales support.

Fastenal generated $266 million in operating cash flow during the quarter and returned $305 million to shareholders, primarily through dividends.

The company expects approximately $320 million in net capital expenditures this year, equal to about 3.5% of projected sales. Spending will support distribution center capacity and automation, FMI devices, and information technology infrastructure.

Tunnicliff said Fastenal was not issuing formal gross-margin guidance. However, he noted that the company’s historical customer-mix pattern has typically produced sequential gross-margin declines of about 10 to 20 basis points during comparable periods.

Management remains focused on maintaining or improving operating margin even as larger strategic accounts account for a greater share of sales.

Florness also tied Fastenal’s financial performance to its employee compensation model. He said incentives based on pretax profit growth extend deep into the organization.

Operating income increased by $65.7 million during the second quarter compared with a $49.2 million increase a year earlier, according to Florness. He said that 33% improvement in profit-dollar growth translated into stronger employee bonuses.

Florness closed his final earnings call by emphasizing the operating principles he said should continue under Watts.

“Love growth, because every problem can be addressed in a simpler way if you’re growing,” he said. “Incrementals matter. It should frustrate the heck out of you if you’re not getting incrementals, especially when you’re growing double digits.”

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: