Why This Matters to Distributors: Motion Industries entering public markets on its own terms — with its own balance sheet and a stated appetite for acquisitions — means industrial distributors should expect one of the sector’s largest competitors to pursue deals more aggressively than it could as part of a company whose other half sells auto parts.

Genuine Parts Co. said the planned spinout of its automotive and industrial businesses into two separate public companies remains on schedule for the first quarter of 2027, after reporting first-quarter results that came in ahead of internal expectations despite a volatile global environment shaped by the conflict in Iran and rising costs across supply chains.

The Atlanta-based company, which operates the NAPA Auto Parts network and Motion Industries — one of the largest industrial parts distributors in North America — confirmed April 21 that the transaction will complete in the first quarter of 2027. President and CEO William Stengel told analysts the response from investors, customers, suppliers, and employees has been broadly positive. “All stakeholders are looking forward to additional details as we advance our planning,” Stengel said.

The two new companies will operate independently with separate leadership, balance sheets, and investor bases. Genuine Parts estimates the ongoing annual cost of running two separate public companies at $100 million to $150 million. That figure covers lost purchasing leverage, duplicated technology and back-office functions, and the cost of building new corporate infrastructure. The costs are divided in half: dis-synergy costs of $50 million to $75 million split evenly between the two companies, and stand-alone operational costs of $50 million to $75 million, the vast majority of which falls on Global Industrial. One-time fees — legal, banking, and professional — are not included in either figure. Stengel said cost estimates are in line with early projections, and the company will share additional details on how existing corporate expenses are allocated between the two businesses in the coming months.

Motion Industries is expected to emerge from the spinout as the more acquisitive of the two companies. Chief financial officer Herbert Nappier told analysts the industrial business will prioritize buying other companies as its primary growth strategy. “When you think about industrial, I think you’ll be thinking about a profile of more M&A,” Nappier said. The automotive business, by contrast, is expected to focus on returning cash to shareholders and investing in its store network. Nappier said both companies are expected to maintain investment-grade credit ratings after the transaction closes.

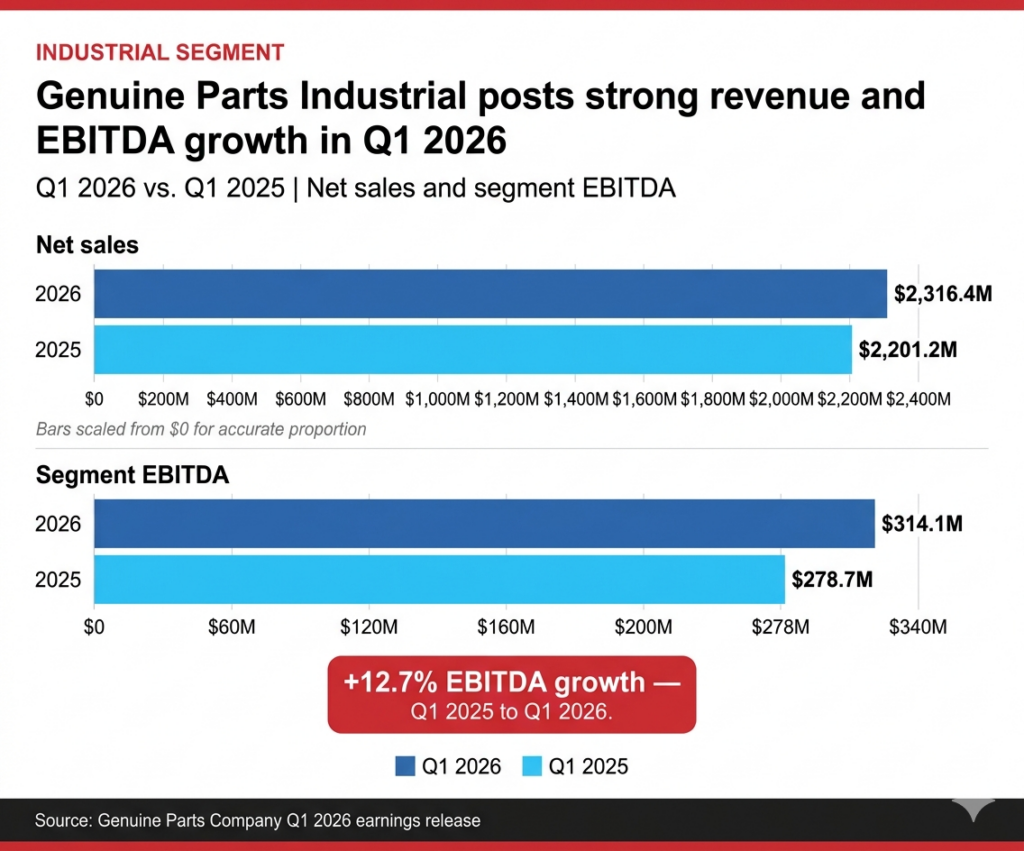

Motion posted a strong quarter heading into the spinout. The segment reported sales of $2.3 billion in the first three months of 2026, up approximately 5% from a year ago, with comparable sales rising approximately 4%. Price increases contributed approximately 3 percentage points of that growth. Segment profit reached $314 million, up 13%, with a margin of 13.6%, a 90-basis point improvement from the same period last year and the strongest margin performance among Genuine Parts’ three business segments.

Sales growth was broad across industrial end markets, with 10 of 14 sectors tracked by the company posting gains in the quarter, up from nine in the fourth quarter of 2025 and just three in the same period a year ago. Food products, automotive, iron and steel, mining and fabricated metals led the gains. Core MRO sales, which account for approximately 80% of Motion revenue, grew more than 5%.

Stengel noted a pickup in customers scheduling planned equipment shutdowns to catch up on deferred maintenance. “We continue to see an increase in planned outage projects to start the year where customers stop operations to do maintenance and repair work as deferred maintenance needs are being addressed,” he said.

For the full company, first-quarter sales reached $6.3 billion, up 6.8% from a year ago, with all three business segments delivering sequential improvement in comparable sales. Despite the stronger-than-expected quarter, Genuine Parts held its full-year guidance unchanged, projecting sales growth of 3% to 5.5%. Nappier said the company deliberately balanced its first-quarter outperformance against a more cautious outlook for the second and third quarters, with the conflict in Iran as the primary variable.

The company is factoring in a $10 million to $20 million profit hit in the second quarter tied directly to the conflict. Higher oil prices are pushing up freight and fuel costs, and the company expects some demand softness as customers navigate elevated energy prices.

“We see some downside risk that we’ve incorporated into our guidance of about $10 million to $20 million of EBITDA as the net negative impact of the conflict to the business,” Nappier said. Genuine Parts said less than one-half of 1% of its total purchases originate from the Middle East, limiting direct supply chain exposure, but the broader effects on global shipping and energy costs are harder to contain. Freight expense represents approximately 3% of total company revenue.

On tariffs, Nappier said the environment has stabilized. Supplier conversations have shifted away from tariff-specific price increase requests toward standard annual negotiations. New steel tariffs under Section 232 have not yet produced significant new cost demands from suppliers.

The NAPA business also had a solid quarter. Sales at company-owned U.S. stores rose 5.5% on a comparable basis, while independent NAPA store purchases grew 1%. Stengel said the mood among independent owners has improved meaningfully, noting that 20 of the largest U.S. NAPA independents visited the company’s Atlanta headquarters two to three weeks before the call. “The tone and the discussions are very positive and optimistic, honestly, sequentially improved,” he said.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: