Why This Matters to Distributors: Home Depot, Lowe’s and Walmart are no longer just retailers competing at the margin of the distribution business. They are making multi-billion-dollar structural moves into the core contractor, MRO, and facility maintenance markets that wholesale distributors depend on — and the pace is accelerating.

A pattern has emerged in American retail that wholesale distributors can no longer treat as background noise. The country’s largest home improvement chains and its biggest mass merchants methodically acquiring, building, and deploying the infrastructure of wholesale distribution — and they are doing it at a scale and speed that independent distributors cannot match through organic growth alone.

The evidence is not anecdotal. It is a string of transactions, product launches, and technology investments that, taken together, describe a coordinated push by Home Depot, Lowe’s and Walmart into the contractor, trades and facility maintenance markets that have historically been the exclusive province of wholesale distributors.

Home Depot: Building a One-Stop Platform for the Pro

No company has moved more aggressively or spent more money pursuing the professional contractor market than The Home Depot Inc.

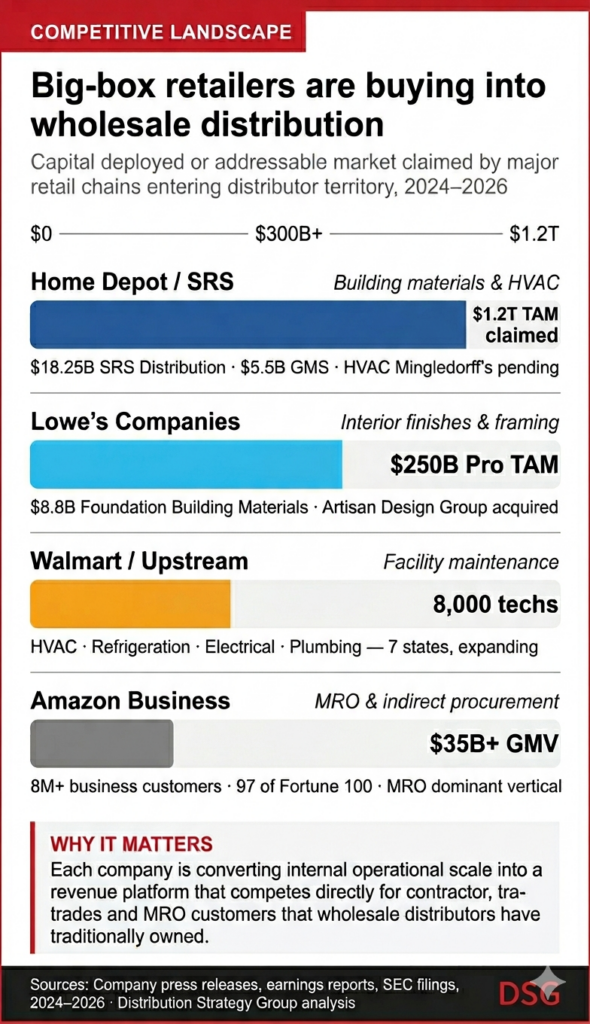

The campaign began in earnest with the $18.25 billion acquisition of SRS Distribution in 2024 — the largest deal in Home Depot’s history — giving the Atlanta-based retailer a specialty distribution network serving roofing, landscaping, and pool contractors. That was followed in September 2025 by SRS completing a $5.5 billion acquisition of GMS Inc., a 300-location distributor of wallboard, ceilings and steel framing serving residential and commercial contractors across North America.

The acquisitions did not slow heading into 2026. In March, SRS announced a definitive agreement to acquire Mingledorff’s Inc., a wholesale distributor of HVAC equipment, parts, and supplies with 42 locations across five Southeastern states. Mingledorff’s, founded in 1939, brings established contractor relationships in a market that Home Depot pegs at $100 billion — and that the company says pushes its total addressable market to $1.2 trillion.

“SRS is a growth engine for The Home Depot, and we continue to drive significant synergies that enable us to bring more innovation and value to our pro customers,” said Ted Decker, chair, president, and chief executive officer of The Home Depot. “The addition of Mingledorff’s will give us an incredible opportunity to build an enterprise-wide platform in HVAC equipment, replacement parts and supplies, creating another entry point into the broader distribution space.”

That last phrase “another entry point into the broader distribution space” — describes exactly what Home Depot is building. Through SRS, it now operates more than 1,250 locations across all 50 states in roofing, building products, interior construction products, landscape, pool and, pending close, HVAC. Each acquisition adds a contractor vertical and the deep trade relationships within it.

The technological investment is accelerating alongside the acquisitions. In April, Home Depot acquired SIMPL Automation, a Waltham, Mass.-based provider of AI-driven robotics and storage systems for distribution centers, to accelerate same-day and next-day fulfillment for professional customers. Home Depot’s Pro segment now accounts for 50 percent of total company revenue, and online B2B sales are outpacing overall digital growth.

Lowe’s: A Different Model, the Same Target

Lowe’s Companies Inc. is pursuing the same contractor market through a parallel strategy, anchored by two major acquisitions completed in 2025: Artisan Design Group, a provider of design, distribution and installation services for interior finishes, and Foundation Building Materials, an $8.8 billion deal adding a distributor of ceiling systems, metal framing, drywall and insulation.

Together, the acquisitions are intended to create what Lowe’s describes as a “comprehensive interior solutions platform” for homebuilders — bundling material distribution with design services and installation support. Pro customers now account for 40 percent of Lowe’s revenue, and the company has stated its ambition to reach a $250 billion total addressable professional market.

“Completing the acquisition of FBM is an important step in accelerating our Total Home strategy to serve large pro customers,” said Marvin Ellison, Lowe’s chairman, president, and chief executive officer. “Together with our recent acquisition of ADG, we are creating a comprehensive interior solutions platform to better serve the homebuilder.”

On the digital side, Lowe’s has expanded its Pro Extended Aisle platform to give contractors access to a broader product catalog, enhanced its quoting and purchasing tools for small and medium contractors, and deepened MyLowe’s Pro Rewards. The company is also pursuing what it calls “agentic commerce,” developing AI-powered capabilities for contractor procurement workflows.

Walmart: The Facility Maintenance Play

While Home Depot and Lowe’s are targeting the building and construction trades, Walmart is moving into the commercial facility maintenance market with a business called Upstream Facility Services, launched publicly in April.

Upstream is built on the maintenance infrastructure Walmart developed to support more than 10,900 of its own stores — HVAC, refrigeration, electrical, plumbing, and general maintenance, delivered by 8,000 technicians positioned near Walmart locations. Walmart notes that approximately 90 percent of the U.S. population lives within 10 minutes of one of its stores, which means its technician network is also within 10 minutes of most of the commercial operators it intends to serve.

The initial target is multi-location operators — quick-service restaurant chains, convenience stores, banks, and light retail — where facility downtime directly affects revenue. Upstream is currently licensed in seven states: Alabama, Arkansas, Louisiana, North Carolina, Oklahoma, South Carolina, and Texas, with expansion described as rapid.

“We’ve spent years building one of the largest in-house facility service operations in the country,” said R.J. Zanes, vice president of Walmart Facility Services. “Upstream takes that capability beyond our walls, combining national scale, skilled technicians and real-time visibility to help businesses run with fewer disruptions.”

What distinguishes Upstream from a conventional service provider is the technology underneath it. Walmart has embedded artificial intelligence and computer vision into its facility operations and built digital twins — detailed 3D models of store infrastructure covering HVAC, refrigeration, electrical and plumbing systems — that allow it to shift from reactive repairs to predictive maintenance.

The Shared Logic Driving All Three

The strategies of Home Depot, Lowe’s and Walmart are distinct in their target markets and methods, but they share a common economic rationale: each company has spent years building operational infrastructure at enormous scale, and each is now converting that infrastructure from a cost center into a revenue-generating platform.

For Home Depot and Lowe’s, the conversion involves using retail scale, brand recognition, and supply chain reach to pull contractors away from independent distributors and into a single-source relationship. For Walmart, it means deploying a technician network and predictive maintenance technology — built and paid for to serve Walmart’s own stores — to compete for the commercial facility maintenance contracts that HVAC, plumbing and electrical distributors have long enabled through their contractor customers.

Amazon Business is also advancing on a parallel track. The company reported more than $35 billion in annualized gross merchandise value through Amazon Business as of mid-2025, serving more than 8 million organizations worldwide, including 97 of the Fortune 100. Amazon Business’s core strength is in MRO, office supplies, and indirect procurement — categories where distributors have historically competed on breadth of catalog and speed of fulfillment.

What It Means for Distributors

The competitive pressure these moves create operate at multiple levels simultaneously. At the customer level, a contractor who begins purchasing roofing materials through SRS, interior finishes through Lowe’s Pro and HVAC supplies through the pending Mingledorff’s platform has fewer reasons to maintain independent distributor relationships across those same categories. The consolidation of purchasing into a single platform is precisely what Home Depot and Lowe’s are selling — convenience, credit, digital tools, and project management bundled together.

At the contractor intermediary level, Walmart’s Upstream model threatens a different but equally important revenue stream. HVAC and electrical contractors have historically been among the most reliable customers for distributors, buying parts and supplies job by job. When Upstream absorbs facility maintenance contracts at multi-location commercial operators and fulfills them through its own supply chain, both the operator and the contractor as a customer disappear from the distributor’s account base simultaneously.

The one constraint these large competitors have not yet solved is the depth of relationship and technical expertise that specialized distributors bring to complex, custom or highly engineered applications. Home Depot’s SRS platform and Lowe’s pro acquisitions are strongest in commodity-adjacent building materials categories. Upstream’s technician model is built for standardized maintenance trades, not highly specialized industrial or process applications. Amazon Business performs best in predictable, repeatable indirect procurement — not in technical sales situations requiring application knowledge.

Distributors whose value proposition is grounded in technical depth, local service responsiveness and engineering support have structural advantages that none of these platforms can replicate on a scale. The distributors most exposed are those competing primarily on price, product breadth and transaction speed in the trades and MRO categories where Home Depot, Lowe’s and Walmart are investing most heavily.

The question is not whether these moves will affect the distribution industry. They already are. The question is which distributors have built the kind of customer relationships and service capabilities that a $1.2 trillion platform cannot replace with a catalog, a technician network, and a digital twin.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: