Why This Matters to Distributors: Walmart is entering the commercial facility maintenance market with 8,000 technicians, AI-powered infrastructure and a geographic footprint that reaches 90% of the U.S. population — and the distributors most exposed serve the exact multi-location operators Upstream is targeting first.

Walmart has launched a commercial facility maintenance business, and the implications for wholesale distributors serving the HVAC, electrical, plumbing and MRO markets are more direct than they may first appear.

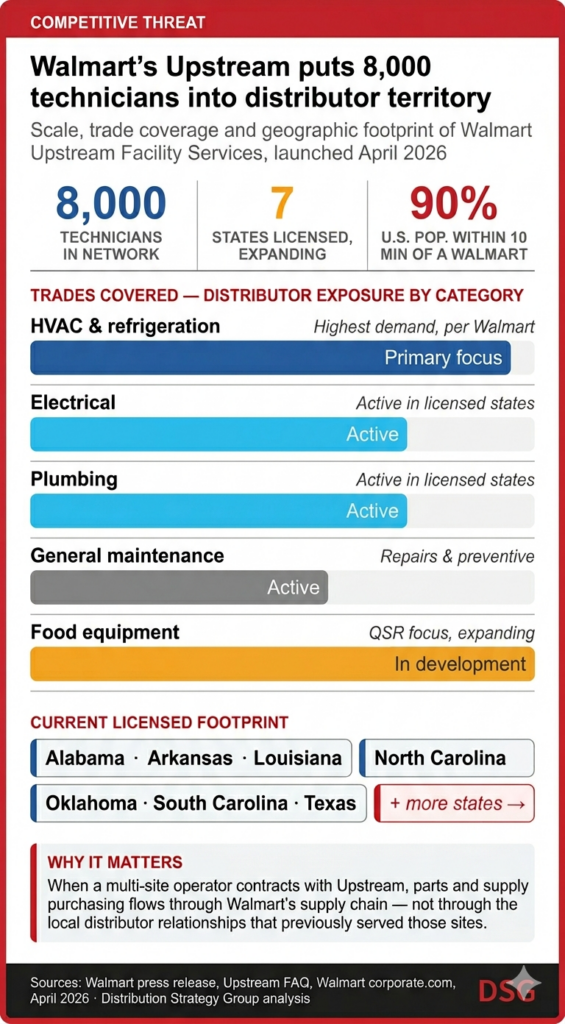

The Bentonville, Ark.-based retailer introduced Upstream Facility Services on April 14, describing it as a business built on the maintenance infrastructure that supports more than 10,900 Walmart and Sam’s Club locations. Upstream currently covers five trades: HVAC, refrigeration, general maintenance, electrical and plumbing. Its model combines urgent repairs, preventive maintenance, and predictive service, backed by a network of 8,000 technicians positioned near Walmart store locations. The service targets businesses operating across distributed, multi-location footprints — specifically quick-service restaurants, retail locations, and banks.

“We’ve spent years building one of the largest in-house facility service operations in the country,” said R.J. Zanes, vice president of Walmart Facility Services. “Upstream takes that capability beyond our walls, combining national scale, skilled technicians and real-time visibility to help businesses run with fewer disruptions.”

Upstream is not a new idea tested quickly. According to Walmart’s own Upstream website, the business is currently licensed and actively serving clients in Alabama, Arkansas, Louisiana, North Carolina, Oklahoma, South Carolina, and Texas, with its footprint described as expanding rapidly. Technicians are positioned near Walmart store locations — a deliberate geographic strategy, given that 90% of the U.S. population lives within 10 minutes of a Walmart store.

The technology backing Upstream goes beyond a dispatch system. Walmart has embedded artificial intelligence (AI) and computer vision into its facility operations and built digital twins — detailed 3D models of its store infrastructure covering floor plans, refrigeration systems, HVAC, and plumbing. That technology supports the shift from reactive repairs to predictive maintenance, allowing Upstream to identify potential failures before they cause downtime.

For wholesale distributors, competitive exposure runs on two tracks. The first is direct. When a multi-site operator — a restaurant chain, a convenience store network, a bank — contracts with Upstream for facility maintenance across its locations, the parts and supplies consumed in that workflow through Walmart’s own procurement channels. The distributor relationships that previously served those sites do not automatically follow the contract. They get displaced.

The second track is less visible but equally significant: the local contractor channel. HVAC and electrical contractors have historically been among the most dependable end customers for distributors, buying parts and supplies on a job-by-job basis as they service commercial accounts. When Upstream absorbs that collaborate with a centralized model with its own technician workforce and supply chain, it removes both the commercial operator and the contractor intermediary through whom distributors often sold.

The geographic concentration of Upstream’s current footprint sharpens the exposure. Alabama, Arkansas, Louisiana, North Carolina, Oklahoma, South Carolina, and Texas are not random markets. They are Sunbelt states with dense concentrations of the quick-service restaurant chains, convenience store operators, and light retail chains that Upstream is explicitly targeting as its first commercial customers.

Upstream’s licensed footprint is still limited to seven states, and Walmart has not disclosed the scale of revenue or number of contracted client locations beyond the 500 sites it quietly served during its one-year pilot period before the public launch. Those are real constraints. Contractor licensing requirements vary by state and by trade — electrical, plumbing and HVAC each carry separate licensing regimes — and expanding nationally means working through each of them.

Walmart also faces a market perception challenge. According to the Upstream FAQ, the service is designed for non-competing commercial operators — quick-service restaurants, convenience stores, and banks. Grocery chains, drug store operators, and other retailers that compete directly with Walmart for consumer spending are not likely targets, and some may actively avoid the arrangement. That limits the addressable market in ways that are not immediately obvious from the headline announcement.

Even so, the infrastructure behind Upstream is not speculative. Walmart built it over years, operating it against the maintenance demands of one of the world’s largest real estate portfolios before offering it externally. The technology, the technician network and geographic density already exist. The question for distributors is not whether Upstream represents a threat — it does — but how quickly it scales past seven states and into the customer categories that represent the most recurring, predictable demand in the facility supply market.

Distributors that have built their businesses around multi-location commercial operators in the South and Southeast are closest to that answer.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: