Why This Matters to Distributors: Falling employment in wholesale trade — even as overall hiring rebounds — signals slowing order activity, continued inventory discipline, and a more cautious outlook across the distribution channel.

U.S. job growth strengthened in March, but the latest data from the U.S. Bureau of Labor Statistics underscores a growing divide between the broader labor market and conditions facing wholesale distributors.

The economy added 178,000 jobs in March, while the unemployment rate held at 4.3%. Hiring gains were concentrated in service-oriented and project-driven sectors, including health care, construction, transportation, and warehousing.

Wholesale trade moved in the opposite direction.

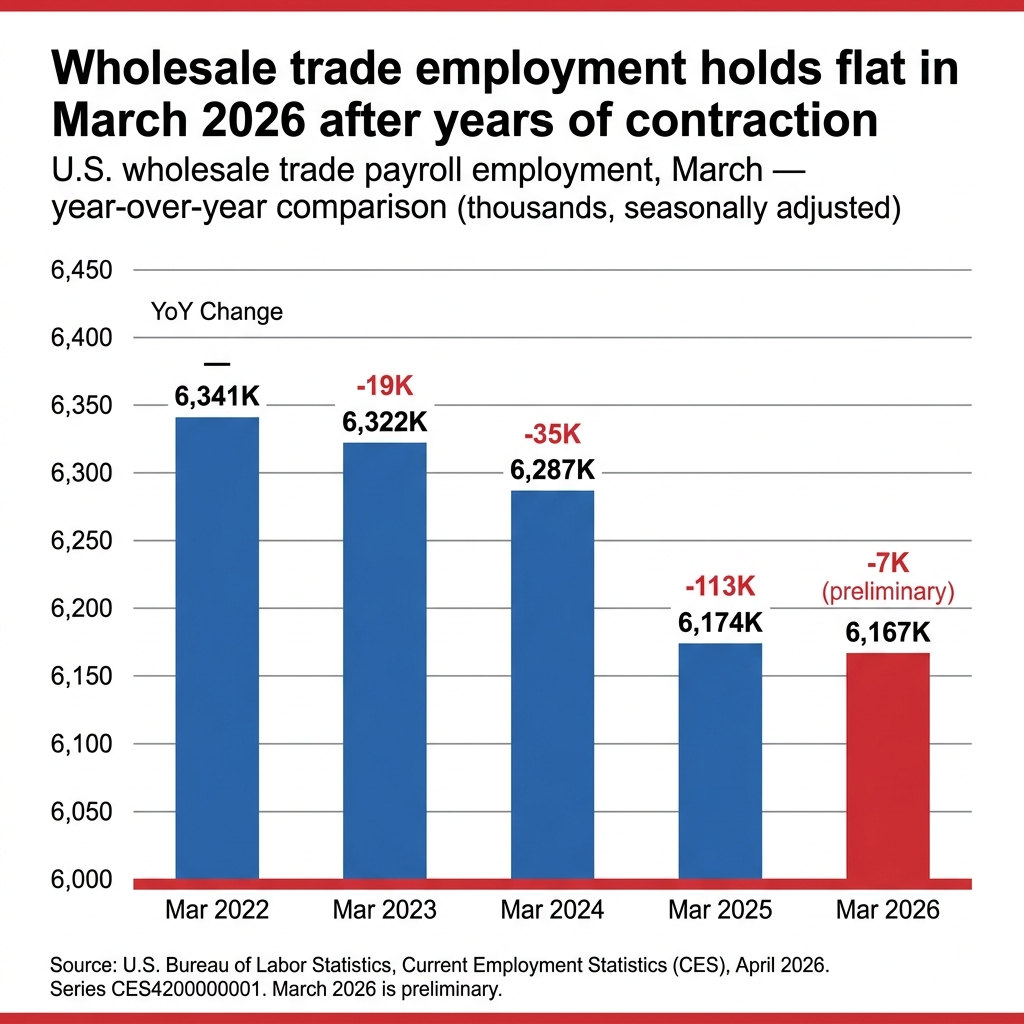

Employment in wholesale trade declined by 13,900 jobs in March, one of the sharper pullbacks among major industries and a notable reversal from the more stable hiring patterns seen earlier in the year.

The decline stands out because it comes at a time when other parts of the goods economy are still adding jobs. Transportation and warehousing employers added 21,000 positions, while construction firms expanded payrolls by about 26,000. That divergence suggests that while goods continue to move through the supply chain, distributors are tightening staffing in response to weaker or less predictable demand.

The data points to a shift in how distributors are managing through current market conditions.

After several years of demand volatility tied to inflation, tariffs and supply chain disruption, many distributors have moved into a more defensive operating posture. Hiring is often one of the first levers adjusted when order visibility weakens or when customers delay purchases. The March decline in wholesale employment indicates that those conditions are persisting — or, in some sectors, intensifying

At the same time, distributors are continuing to invest in operational efficiency, including automation, digital ordering and AI-driven tools that reduce reliance on labor in areas such as customer service, quoting, and warehouse operations. While those investments are long-term in nature, they are increasingly intersecting with near-term cost control efforts, allowing companies to manage volume fluctuations without adding headcount.

The broader labor report reinforces that caution.

Labor force participation edged down to 61.9%, and wage growth slowed to 3.5% year over year, both signs of a labor market that is losing momentum. For distributors, slower wage growth may provide some relief after several years of rising labor costs, but it also reflects softer overall demand conditions that can weigh on sales volumes.

The contrast between wholesale job losses and gains in transportation and warehousing also highlights a structural shift underway in the distribution landscape. Logistics providers — including parcel carriers and third-party operators — continue to expand capacity, particularly as they push deeper into B2B delivery. That expansion is capturing a larger share of fulfillment activity, even as distributors themselves remain cautious on staffing.

For wholesale distributors, the employment data serves as an early indicator of broader business conditions.

Sustained declines in wholesale employment typically align with slower order growth, tighter inventory management, and increased pricing pressure. Conversely, a stabilization in hiring would signal improving confidence in demand and replenishment cycles.

For now, the March report suggests that distributors are still in a holding pattern — maintaining service levels and fulfillment capacity while limiting incremental labor costs.

The headline job gains point to a labor market that remains resilient. But within wholesale trade, the message is more restrained: distributors are preparing for a period of uneven demand and continued margin pressure, even as activity elsewhere in the economy remains comparatively strong.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: