Why This Matters to Distributors: DNOW’s transformation from a debt-free, $599 million revenue business one year ago into a $1.18 billion combined operation carrying $455 million in net debt illustrates the operational and financial weight of large-scale consolidation in the pipe, valves and fittings segment and the execution demands that follow when two companies with different enterprise systems, customer bases and end markets merge under one roof.

DNOW Inc. posted first quarter 2026 revenue of $1.18 billion and a net loss of $44 million as the Houston-based industrial pipe, valves and fittings distributor absorbed the first full quarter of its merged operations with MRC Global and pushed into two growth markets it had not pursued at meaningful scale: data centers and midstream natural gas infrastructure.

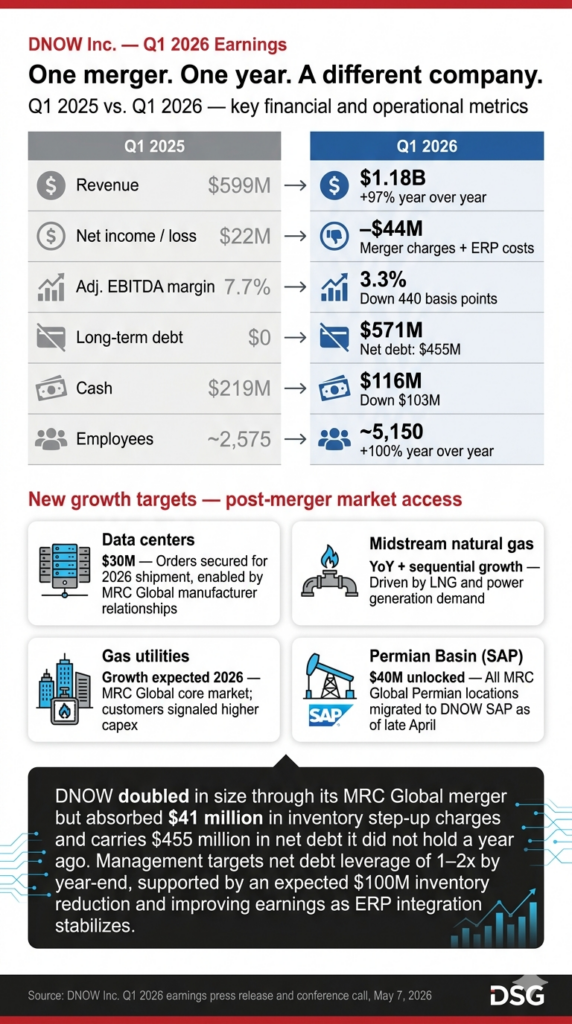

The results mark a sharp contrast to the first quarter of 2025, when DNOW reported $599 million in revenue, $22 million in net income, no long-term debt and $219 million in cash. On March 31, the company carried $571 million in long-term debt and $116 million in cash, producing net debt of $455 million.

The net loss reflected $41 million in inventory step-up charges tied to the merger, elevated selling, general and administrative expenses, and continued spending to stabilize MRC Global’s Oracle enterprise resource planning platform.

David Cherechinsky, president and chief executive officer, said the first quarter represented a low point. “I am confident that the overall DNOW business has bottomed out in 1Q 2026,” Cherechinsky said on the company’s May 7 earnings call. He called 2026 a transition year and said meaningful earnings improvement would accelerate into 2027.

The enterprise resource planning stabilization effort remains the dominant operational challenge. MRC Global’s U.S. platform supports half of DNOW’s U.S. revenues and 42% of consolidated global revenue. Disruptions on that system contributed to a $128 million year-over-over-year first quarter revenue decline on a combined-company basis, with upstream and downstream markets absorbing the steepest declines.

The company is running parallel tracks: stabilizing the legacy MRC Global Oracle system while migrating 20 U.S. MRC Global locations focused on upstream and midstream activity to DNOW’s SAP platform.

As of late April, all MRC Global Permian Basin operations completed the SAP migration. Cherechinsky said the conversion is already generating commercial results. “We now have easy access to approximately $40 million of additional MRC Global inventory that is now visible and deployable, supporting faster fulfillment and improved service levels,” he said. He described the unlocked inventory as “a powerful commercial lever, giving us speed to customer advantage.”

Stabilization efforts carry a defined and recurring cost. Cherechinsky said DNOW is spending approximately $4.5 million per quarter on teams dedicated to the MRC Global platform, with another $4 million per quarter in overtime, temporary workers, and additional warehouse personnel. The temporary labor headcount has declined from 200 additional employees in the prior quarter to approximately 115. The $4.5 million quarterly stabilization cost is expected to remain stable through year-end, and workforce-related costs are expected to moderate.

Data centers represent the first new growth market. Cherechinsky said DNOW has secured approximately $30 million in data center orders expected to ship in 2026, supplying pipe, valves and fittings for cooling systems and associated infrastructure. The business would not have been accessible without the merger. “We were able to do so because of MRC Global’s connections with manufacturers, relationships DNOW didn’t have,” he said.

Midstream natural gas infrastructure is the second. Cherechinsky cited rising power generation demand, liquefied natural gas export activity and data center load growth as drivers of sustained midstream investment. DNOW grew year over year and sequentially in midstream during the first quarter and expects the sector to be a primary source of revenue recovery and market share gains. Gas utilities, a market MRC Global had cultivated as a core business, are also a near-term growth target. “Gas utilities distribution is the sector that MRC Global pioneered and expertly cultivated in the market very well,” Cherechinsky said. Several gas utility customers have signaled increases in longer-term capital spending.

In February, DNOW completed its acquisition of Edge Controls for $46 million, an automation and controls business the company is integrating into its Process Solutions platform. Edge Controls designs and installs programmable logic controllers, touchscreens and supervisory control and data acquisition systems across energy, industrial and infrastructure markets. Cherechinsky said the capabilities translate directly to data center applications with minimal modification.

DNOW raised its annualized synergy target to approximately $30 million, up from the $17 million run rate it had previously expected to achieve by the end of the first year. The three-year annualized synergy target of $70 million remains unchanged. The company repurchased $50 million in shares during the quarter, its largest buyback quarter on record, using debt to fund repurchases for the first time in its history. Management is projecting net debt leverage in the 1 to 2 times adjusted earnings before interest, taxes, depreciation, and amortization range by year-end, supported by an expected $100 million inventory reduction in the second half of the year.

U.S. revenue for the quarter was $985 million, up from $474 million a year earlier. Canada contributed $51 million, down from $62 million. International revenue reached $147 million, up from $63 million in the year-ago period.

For distributors operating across upstream energy, midstream gas infrastructure or industrial end markets, DNOW’s post-merger positioning signals where the company expects to compete: broader inventory depth, faster fulfillment enabled by a unified enterprise resource planning platform and automation and controls capabilities that extend its reach into infrastructure-intensive markets neither legacy company could have addressed alone. Whether the company converts that platform into recovered margins and returns to the profitability profile it carried 12 months ago is the central question heading into the second half of 2026.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: