Why This Matters to Distributors: New U.S. metals tariffs, persistent supplier cost inflation and uneven lead times are raising the cost to serve customers across the MRO channel, forcing distributors to sharpen pricing, sourcing, and inventory strategies.

Industrial supply and maintenance, repair and operations (MRO) distributors entered the second quarter expecting more stability after several years of disruption tied to inflation, freight volatility, and uneven demand. Instead, they are confronting a new round of cost pressure tied to U.S. tariff changes, higher metals prices and continued supply chain variability.

The result is a more complex operating environment heading into summer, where demand remains intact but the cost to serve customers is rising.

The Institute for Supply Management said its manufacturing PMI rose to 52.7 in March, the third consecutive month of expansion. At the same time, customers’ inventories remained in “too low” territory, indicating continued demand for maintenance supplies and industrial consumables. ISM also reported that 64% of manufacturer comments in March were negative, with 20% citing tariffs and about 40% citing geopolitical disruption, including conflict in the Middle East.

For distributors, the issue is not demand. It is the growing difficulty of maintaining margins as costs shift across a broad range of products.

The most immediate change came from Washington. A presidential proclamation signed April 2 and effective April 6 modified how Section 232 tariffs apply to steel, aluminum, and copper imports. Under the updated rules, duties apply to the full customs value of covered imports rather than only to the value of the metal content in many cases.

That shift increases exposure across a wide range of industrial products.

MRO distributors are particularly exposed because a large share of their catalogs consists of metal-intensive goods, including fasteners, fittings, valves, conduit, couplings, bearings, brackets and cutting tools. Even where tariff rates are unchanged, the move to full-value assessment can increase total duty costs.

The policy includes exemptions for products with minimal metal content and a transitional rate for certain industrial and electrical equipment. But for many core MRO categories, the immediate effect is higher landed cost and more complex pricing decisions.

Public distributor commentary suggests these pressures were already building before the tariff change.

In a 2025 earnings call, Grainger CEO D.G. Macpherson said the company had gone through “over a thousand negotiations” with suppliers, adding, “That’s not normal, for the record.” The comment reflects the scale of supplier-driven pricing activity across the industrial supply base.

MSC Industrial has also cited elevated input costs. The company said in a recent earnings call that tungsten — a key input for carbide cutting tools — had increased more than 100% and affected a meaningful portion of its business. Executives said the company has been implementing mid- to high-single-digit price increases from suppliers and expects continued pressure.

Those dynamics extend beyond individual companies.

Copper, a critical input across electrical and mechanical MRO products, remains under pressure. Industry forecasts, including from the International Copper Study Group, indicate that the global refined copper market is expected to be in deficit in 2026 as demand tied to electrification, infrastructure and data centers continues to outpace supply growth.

For distributors, copper’s impact is broad. It affects pricing across wire and cable, motors, fittings, and other high-volume maintenance categories. Unlike specialty materials, copper-related products are often treated as routine purchases by customers, which can make price adjustments more difficult to absorb.

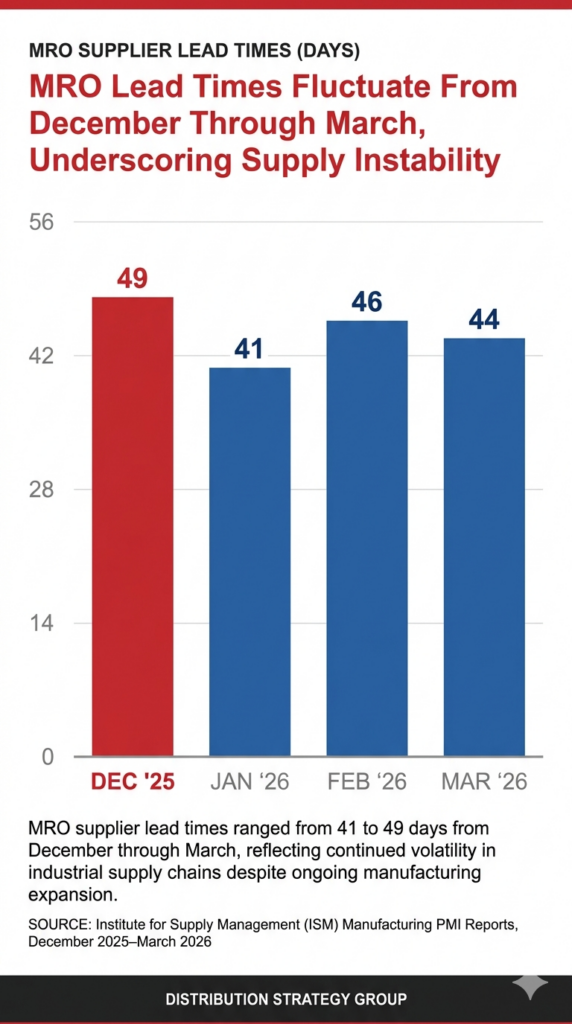

Lead times remain another variable.

ISM data shows supplier delivery times for MRO-related goods remain elevated compared with pre-pandemic norms. While March showed some improvement from earlier in the year, conditions remain uneven, reflecting ongoing supply chain disruption and supplier caution.

For distributors, variability matters as much as direction. Unpredictable lead times complicate inventory planning, service levels, and customer commitments, particularly in environments where downtime carries significant cost.

In response, distributors are adjusting operations in several ways.

“Our customers are expecting an even higher level of execution on our value proposition, to bring solutions that make them better and more profitable. They face the same challenges around cost, margin, and inventory,” said Stellar Industrial Supply senior vice president of customer experience Molly Langdon. “For us, that means a more intense focus on cost savings for them – process improvement or alternative methods and tools that can help them through profitability pressures or threats to production.”

First, tariff classification has become a commercial priority. With duties tied more directly to product composition and value, distributors are reviewing SKUs to determine exposure and adjust pricing accordingly. Faster and more accurate classification can help limit margin erosion.

Second, inventory strategies are becoming more targeted. Rather than broadly increasing stock, distributors are focusing on high-risk, high-velocity items where supply constraints and cost pressure are most pronounced, including metal-intensive products and cutting tools.

Third, vendor-managed inventory and vending programs are gaining importance. These models provide real-time consumption data, allowing distributors to align replenishment more closely with actual usage. In a constrained supply environment, that visibility can improve allocation decisions and reduce stockouts.

Finally, distributors are taking a more consultative approach with customers. As costs rise and availability shifts, customers are seeking guidance on alternatives, timing, and sourcing. Distributors that can help customers navigate those decisions may strengthen relationships even as pricing pressure persists.

The current environment does not reflect a collapse in industrial demand. Instead, it reflects a tightening in the economics of distribution.

Tariffs have increased cost complexity. Metals inflation continues to affect key categories. Supplier pricing remains active. And lead times, while improving in some areas, are still inconsistent.

For MRO distributors, the challenge is balancing those pressures without disrupting service.

That means managing pricing more precisely, sourcing more flexibly and aligning inventory more closely with risk. It also means responding quickly as conditions change.

The distributors that execute on those fronts will be better positioned as the market moves through the remainder of 2026.

“We continue to see the demand from our customers and cost pressure from suppliers. There isn’t really a time where we don’t feel margin pressure, but more so during these times of volatility. The tariff situation was a reminder to us that we have to be quick, intentional, and accurate when it comes to protecting margin,” Langdon said. “We cannot wait – on behalf of ourselves and our customers. Having automated or dynamic mechanisms around pricing allows us to respond more effectively, reducing risk of eroding margin.”

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: