Why This Matters to Distributors: Branch traffic is improving, but the signal is incomplete — distributors seeing higher in-branch activity may still face uneven demand as ecommerce growth and channel shifts dilute the link between foot traffic and overall sales.

Branch traffic across major industrial distributors improved in March, offering a cautiously positive signal for demand trends after a slow start to 2026, according to a research note from Jefferies.

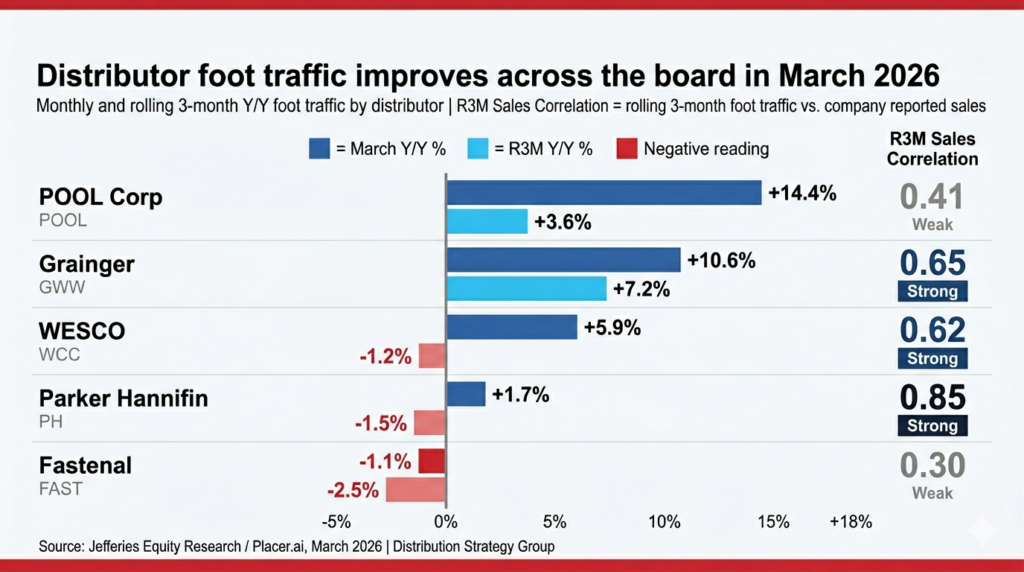

In an April 10 report, analysts Stephen Volkmann, Chirag Patel and Jamie Simonson said monthly traffic increased sequentially across several distributors, including W.W. Grainger, Wesco International and Parker Hannifin’s Parker Stores.

The firm said the data — sourced from Placer.ai and based on anonymized cellphone geolocation signals from about 25 million devices — is aggregated across each company’s branch network. Jefferies said it cannot see individual device pings or specific branch locations, and it does not break out results by region. The data set includes only branches open for at least 12 months, making it a same-store measure of traffic across established locations.

Jefferies described the data as a “big picture” indicator of overall branch activity rather than a precise measure of sales. It also does not capture ecommerce or other non-branch channels, which are an increasing share of distributor revenue.

Even with those limitations, March showed improvement. Grainger’s local same-branch visits rose 10.6% year over year, up from 10.0% in February. Wesco’s visits increased 5.9% after a 1.7% decline the prior month, while Parker Stores posted 1.7% growth.

The analysts said the results reflect “an encouraging trend of momentum” across industrial and specialty distribution, but they emphasized that a broader inflection in fundamentals has not yet occurred.

“While fundamentals have still yet to meaningfully inflect, we continue to see growing signs of a recovery,” the analysts wrote, pointing to recent expansionary readings from the Institute for Supply Management and stronger manufacturing activity reported by Fastenal in February.

Jefferies said the usefulness of traffic data as a leading indicator varies by company. Parker Store traffic shows a 0.85 correlation with rolling three-month sales trends in Parker Hannifin’s North America industrial segment, while Grainger’s traffic shows a 0.65 correlation with sales growth and 0.73 with volume growth.

For Wesco, traffic has a 0.62 correlation with sales in its Electrical and Electronic Solutions segment, which accounts for about 40% of total revenue, though the relationship has been more volatile since the pandemic.

By contrast, Fastenal’s March visits declined 1.1% year over year, compared with a 1.0% gain in February. Jefferies said traffic has only a 0.30 correlation with Fastenal’s sales, reflecting the company’s shift toward onsite locations, vending and ecommerce — channels not fully captured in branch-level data.

Pool Corp. recorded the strongest monthly traffic gain at 14.4%, though Jefferies said its traffic-to-sales correlation is weaker at 0.41.

Jefferies said monthly data provides a more real-time view of activity, but it relies more heavily on rolling three-month comparisons to assess how closely traffic aligns with quarterly sales.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: