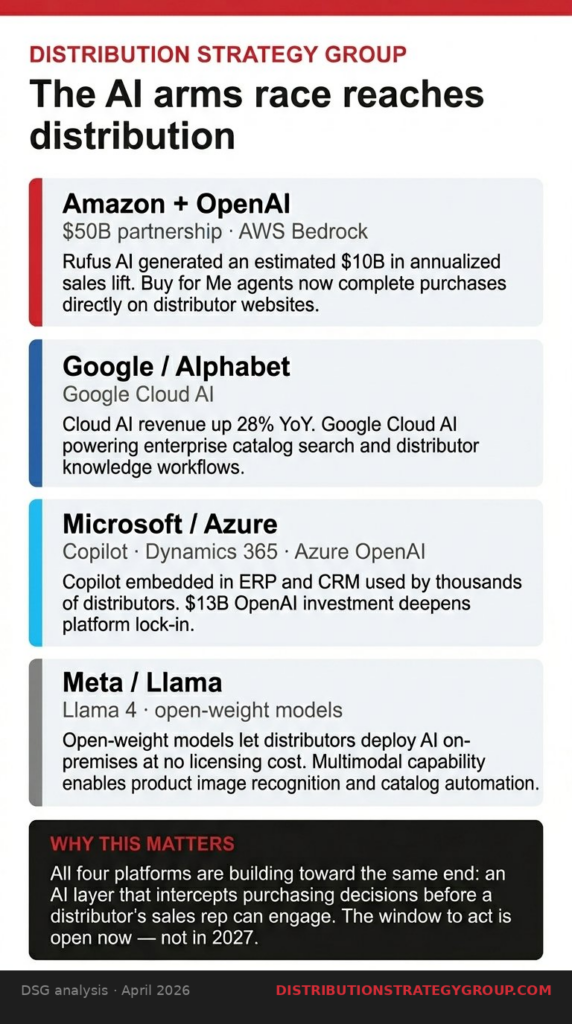

Why This Matters to Distributors: The seven largest AI companies are no longer building for researchers — they are building for the enterprise workflows distributors run every day, and the distributors that connect AI to real operations in the next 12 to 18 months will be measurably harder to compete against by 2027.

The seven largest artificial intelligence companies do not agree on much. They compete for talent, customers, computing capacity, and market position. But their announcements last week pointed in the same direction: enterprise AI is leaving the experimental phase.

The market is moving from one-off AI interactions toward systems that perform sustained, multistep work inside the software companies already run. For wholesale distributors, the window for watching from the sidelines is closing faster than most realize.

Anthropic made two of the week’s sharpest moves. On April 16, it introduced Claude Opus 4.7, built for coding, agent tasks, vision, and complex multistep reasoning and not conversation. Four days later, Anthropic announced it was expanding its infrastructure partnership with Amazon for up to 5 gigawatts of new compute capacity.

That number is worth pausing on. Five gigawatts is not a product roadmap item. It is an infrastructure commitment that signals Anthropic expects enterprise demand to scale far beyond what current systems can handle. The company also kept its Mythos Preview model under gated access, though Reuters reported that Mythos’ ability to identify software vulnerabilities has drawn scrutiny from regulators and financial institutions.

For distributors, Anthropic’s direction points to AI that is becoming genuinely useful in sustained, complex work — inside sales support, technical documentation, product-data cleanup, enterprise resource planning and customer relationship management search, contract review, and software integration — rather than tasks that take one prompt and return one answer. The regulatory attention around Mythos also carries a practical message: as models get more capable, governance, access controls and security review become non-negotiable inside any organization that deploys them on a scale.

OpenAI is making an identical enterprise push, but with a sharper emphasis on getting AI into actual workflows rather than just into contracts. OpenAI is expanding deployment partnerships with Accenture, Capgemini, CGI, Cognizant, Infosys, PwC, and Tata Consultancy Services specifically to accelerate enterprise adoption of Codex, its software-automation product. OpenAI is also launching Codex Labs, which embeds specialists directly inside client organizations to integrate Codex into real operations.

Weekly Codex usage has climbed past 4 million developers, up from more than 3 million earlier this month. OpenAI is not waiting for enterprises to figure out implementation on their own. It is sending people in to do it with them.

That matters to distributors because the same implementation gap exists in distribution. Most distributors have software enterprise resource planning, customer relationship management, ecommerce platforms, and pricing tools. What they lack is the connection between those systems and an AI player that can act on the data inside them. OpenAI’s Codex push is a preview of where enterprise AI competition is heading not which model is smartest, but which vendor helps a company get AI running inside real workflows the fastest.

OpenAI also expanded its cybersecurity work. Reuters reported April 14 that the company introduced GPT-5.4-Cyber for vetted security professionals and broadened its Trusted Access for Cyber program with new access tiers. Stronger models mean stronger attack surfaces. That is a direct operational concern for distributors running customer portals, electronic data interchange connections, online ordering systems, and connected warehouse infrastructure.

Google’s recent product updates follow the same logic. As of April 15, Google Cloud’s Gemini Enterprise allows users to register and manage AI agents hosted on Vertex AI Agent Engine across projects — meaning a company can run multiple specialized agents from a single governed platform rather than managing them separately. Google is not selling a smarter search box. It sells a platform for orchestrating AI agents tied to significant business data and workflows.

That architecture fits the distribution problem well. A mid-size distributor might need one AI agent to search product content, another to pull customer account history, another to surface open service issues and another to flag pricing anomalies. Today those are four separate problems. Google, and increasingly every major AI vendor, is building the infrastructure to connect them under one governed layer. The question for distributors is not whether that infrastructure will exist. It already does. The question is who inside the organization is accountable for using it.

Microsoft is making the same argument through the software stack distributors already have. On April 21, the company announced that CBIZ, a business services firm, would use Microsoft Foundry, Microsoft 365 Copilot and Copilot Studio to build what it called an “agent-native operating platform.” The relevance to distributors is direct. Most distributors already run Microsoft through email, collaboration, spreadsheets, and analytics. Microsoft’s current strategy is not to sell a new AI product.

It is to embed governed AI agents into tools distributors are already paying for and already using every day. The upgrade path is shorter than most distribution technology leaders recognize.

Amazon Web Services is attacking what could become the defining enterprise AI problem of the next two years: sprawl. AWS announced April 9 that Agent Registry inside its AgentCore platform is now available in preview — a centralized place to discover, share and govern AI agents across an enterprise. AWS also confirmed that Anthropic’s Claude Mythos Preview is available inside Amazon Bedrock through a gated program called Project Glasswing. The message is that AWS wants to be both the deployment environment and the governance layer for enterprise AI at scale.

Distributors that have already run AI pilots know exactly what sprawl looks like. A customer-service tool here. A pricing tool there. A product-search experiment somewhere else. No common data layer. No shared governance. No way to measure whether any of it is actually working. AWS is building the infrastructure to solve that problem. Distributors that wait until sprawl becomes unmanageable before addressing it will spend more time and money cleaning it up than they would have spent getting it right from the start.

Nvidia’s announcements reinforce where the real competition is heading. The company is positioning itself for a market in which AI agents move continuously among enterprise applications, performing work on behalf of users in real time. Nvidia also released an open Agent Toolkit for building and running those agents. The competitive battleground is no longer which company trains the biggest model. It is which company deploys agents most efficiently inside live business operations — and which distributors have the data infrastructure ready to support them.

Meta’s moves are the furthest from direct distributor relevance but carry an important signal. Reuters reported on April 8 that Meta unveiled Muse Spark, the first model from its superintelligence team. Meta extended its custom chip partnership with Broadcom through 2029. Distributors are unlikely to buy Meta’s enterprise AI tools directly. But when the company building Facebook and Instagram is making 2029 chip commitments to support its AI ambitions, it is a useful indicator of how long and how seriously the largest technology companies expect this buildout to run.

Taken together, last week’s announcements from all seven companies tell a consistent story. Enterprise AI consolidates around three priorities: agents that perform sustained work, governance that keeps humans in control of what matters, and integration that connects AI to the systems companies already run. The best positioned distributors for that environment are not the ones with the most AI experiments. They are the ones that have identified the two or three workflows where AI produces measurable results — quote turnaround, customer-service resolution, product-data accuracy, inside sales productivity — and are building toward those outcomes with real accountability and real metrics.

The risk is not moving too fast. It is moving too slowly while the infrastructure matures around you and arriving late for an operating model that competitors have already built.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: