Why This Matters to Distributors: Apollo’s investment strengthens one of the largest contractor platforms in the country and increases the likelihood of additional acquisitions and purchasing consolidation. As more contractors join large, private equity-backed organizations, distributors will face growing pressure to serve customers that buy at scale, negotiate nationally, and expect sophisticated procurement capabilities.

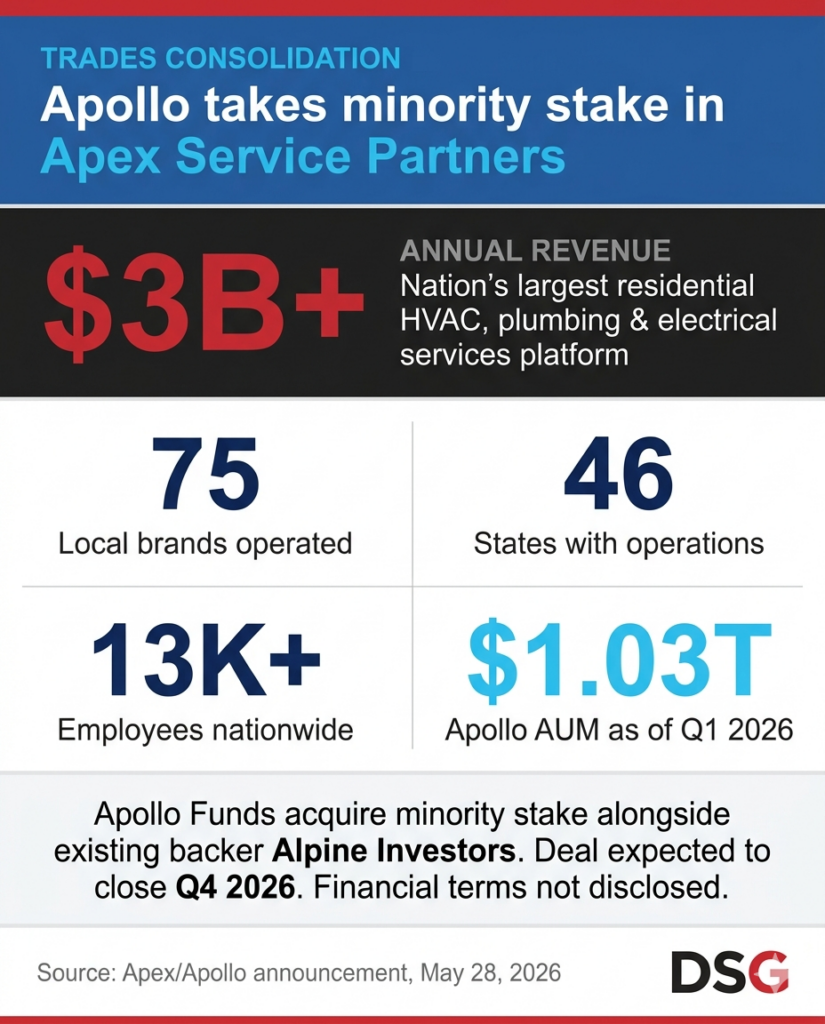

Apollo Global Management has agreed to acquire a minority stake in Apex Service Partners, providing fresh capital to the nation’s largest residential HVAC, plumbing and electrical services platform and reinforcing the growing influence of large, private equity-backed contractor organizations across the residential trades market.

The transaction brings Apollo Funds alongside existing investor Alpine Investors, which is also increasing its investment in Apex. Financial terms were not disclosed. The deal is expected to close in the fourth quarter of 2026.

Founded in 2019, Apex has grown into one of the largest residential services companies in the U.S through a combination of acquisitions and organic expansion. The company operates 75 local brands across 46 states, employs more than 13,000 technicians and support personnel, and generates more than $3 billion in annual revenue.

While the investment represents another major private equity transaction in the home services sector, its significance for distributors extends beyond ownership changes.

The deal provides additional capital to a contractor platform that already commands substantial purchasing volume across HVAC equipment, plumbing products, and electrical supplies. As Apex continues to acquire contractors and expand into new markets, distributors can expect further consolidation of purchasing activity among some of their largest customers.

That trend is reshaping how distributors compete in residential trades markets.

For decades, many distributors built their businesses around relationships with locally owned contractors that made purchasing decisions at the branch level. As contractors join larger platforms, those decisions increasingly shift to centralized procurement teams that evaluate suppliers based on pricing, inventory availability, geographic coverage, technology capabilities, and service performance.

As a result, distributors that once managed dozens of independent contractor relationships may increasingly find themselves negotiating with a smaller number of large organizations that control purchasing across multiple states and markets.

Apex’s scale has already given the company major influence within the supply chain. The company serves millions of residential customers annually and operates across every major U.S. market. Additional acquisitions supported by Apollo’s investment could further increase its purchasing leverage with manufacturers and distributors.

The transaction also highlights the continued flow of institutional capital into residential services. Apollo manages approximately $1.03 trillion in assets, making it one of the largest alternative asset managers in the world. Its investment in Apex reflects growing confidence among institutional investors that residential repair, replacement and maintenance services offer attractive long-term growth opportunities.

For distributors, which means contractor consolidation is likely to continue.

Large contractor platforms backed by private equity have become increasingly active acquirers in HVAC, plumbing and electrical services, creating organizations with broader geographic reach, larger purchasing budgets, and more sophisticated procurement operations. Those platforms often seek standardized supplier relationships and national purchasing agreements that can alter traditional distributor-contractor dynamics.

The trend presents opportunities for distributors with national or multi-regional footprints that can support centralized purchasing programs and consistent service across markets. At the same time, it creates challenges for distributors that have historically relied on local relationships and independent contractor accounts.

Apollo’s investment does not change the market overnight. It does, however, provide another indication that large-scale investors continue to view residential trades as a fragmented industry with significant consolidation potential. As more capital enters the sector, distributors should expect larger contractor organizations to account for an increasing share of industry purchasing volume.

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: