In mature B2B markets, many firms are sales driven. While this configuration has worked well in the past, new business models are emerging that challenge the sales culture and, eventually, take business from a sales-intensive model with better pricing and higher quality product(s) or service(s). In this article, we detail the problems of sales cultures in mature B2B markets, how to identify them, and what needs to be done to move to a market driven culture for better growth and profits.

Looking Through the Rear View Mirror to the Road Ahead

Merchant wholesale distribution for B2B/B2C markets was approximately $8 trillion in sales for 2024, according to the U.S. Census Bureau. The sector represents tens of thousands of firms across some four dozen vertical markets. The industry, depending on the sector, is 75 to 150 years old. Distributors of B2B products can trace their beginning to the Civil War and the rise of the Gilded Age.

Since inception, distribution has been sales-intensive and sales-driven. The need for outside sellers, in the early years, was keen. There was no other way to get product knowledge to customers and understand their needs.” Paper cataloging emerged some 50 years later with the advent of Grainger’s “Motor Book” in 1927. More recently, an online catalog has been building for the last two decades where, today, 30% of wholesale sales are transacted electronically.

Today, despite cataloging and electronic commerce, many wholesalers still rely on outside sales as the primary path to market. Sellers cover geographic territories and have significant input into decisions on products, pricing, and support services. Newer models of business, including Amazon Business, Amazon.com, and Zoro Tool (part of W.W. Grainger), have grown faster in sales than traditional merchant wholesalers. Amazon.com Inc., including the Amazon Business B2B marketplace and Amazon.com, posted a compound annual growth rate of 17% for the past five years, while Zoro Tool has a 10% CAGR since its launch in 2011. By contrast the CAGR for merchant wholesalers overall is just over 4% during this decade.

Additionally, home improvement retailers Home Depot and Lowe’s have in the past decade acquired in the sector and are developing less sales-intensive efforts. For instance, Home Depot is developing flat-bed distribution centers (FDC) that deliver direct to contractors, and project ultimately operating about 150 such facilities. The upshot is that digital models, new models, and hybrid models are growing faster than traditional sales driven merchant wholesaling.

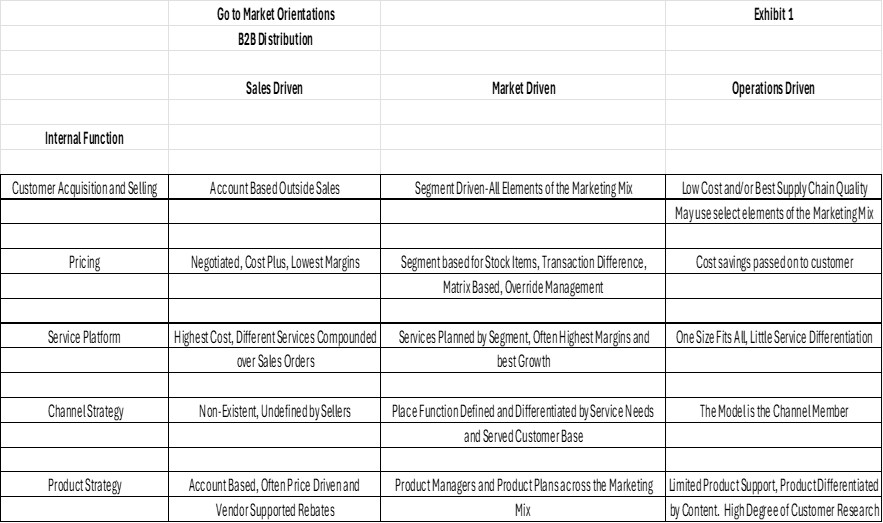

In our work, we find many traditional distributors deny they are sales-driven or a sales culture. The following table (Exhibit 1) sheds light on the go-to-market orientation of the firm whether sales-driven, market-driven, or operations-driven. From a definition perspective, the growth orientation of wholesale firms is:

- Sales-Driven: Outside and inside sales represent the predominance of written orders with sellers controlling or having significant input into price, delivery, payment terms, and special handling, etc. Sales growth is established by individual attention from customers across all parts of the firm’s services and product capabilities.

- Market Driven: Orders are better balanced between sales and electronic commerce with segment-based marketing driving a matrix pricing strategy, segment-based service platform, and product management efforts specific to the segment. Sales growth is accomplished through segment differentiation of the marketing mix.

- Operations-Driven: Orders can be taken either by sellers or electronic commerce. Attention is on limiting or streamlining support services, optimizing physical locations, tight control on inventory in stock, and limited variation on products and services for customers. Operating efficiencies are often passed on as cost-savings to the customer to grow sales.

In the exhibit, the function of the firm on the far left is followed by a brief description under the orientation of the firm. For instance, in pricing, the sales-driven firm is mostly cost-plus, the market-driven firm varies pricing by segment or transaction type, and the operations-driven firm passes efficiencies on to the market to gain share.

Sales-driven firms also have a limited discernable channel strategy, and product-based efforts are made by sellers at the account level. The focus is on the account, not the channel. In our activity costing work, we often find special services offered to small customers, which makes the activity profit dismal.

The upshot is that service provision, who does or does not get a service, saps account profitability. Sellers often do not charge for services and confuse their value with the product and unknowingly commodity the service. In a recent customer audit, we found instances where freight outbound was at the discretion of the outside seller. Small customers, whose activity profit was negative, were often not charged outbound freight. These customers, historically, did not offer top-line growth.

The upshot of the various orientations, from a profit perspective, is that market-driven firms are often in the 8% or greater NOPBT (Net Operating Profit Before Tax and as a percentage of top-line sales), versus operations-driven firms in the 6% or so NOPBT range and sales-driven firms in the 3% to 5% range. Outside selling is expensive and, combined with the custom product/service bundle fomented by seller perceptions, operating expenses are always proportionally greater in sales-driven firms versus marketing or operations orientations.

Sales Myopia and Commodity Hell

Salesforce efforts concentrate on existing products and their functionality. The better sales forces are product-driven and can recite the features and benefits of the products they sell.

More recently, in the past two decades, distributors have added services from distributor warehouse to customer warehouse to add value. Inventory management services (VMI, Integrated Supply, Vending) and a host of other services, including repair and testing, have been mined by distributors to add value to increasing commodity products. However, today, these services are mostly commodities. They can be purchased from most distributors and of equal quality.

The upshot is that there is a dearth of different product and service offerings at the distributor level. Most firms sell the same product(s) and services while touting their differences. But mostly, they sell commodities and, in the words of Jeff Immelt, former CEO of GE, find themselves in a “commodity hell.”

The best way out of this “hell” is first definition and then innovation. Distributor sellers are myopic in nature. Take an industrial and safety distributor that sells drills and gloves. Any number of distributors or new age models can supply these, hence the commodity status. However, if the distributor expands the market definition to recognize that customers don’t necessarily want drills, they need holes. Or that customers don’t necessarily want gloves, they need hand protection. Then the redefinition expands the customer opportunity.

A case in point is a table saw and risk of injury. Instead of wearing cut-resistant gloves, there is technology that shuts down the saw blade and retracts the instant flesh is encountered. The technology is based on an electrical current that passes through the blade.

SawStop, a company near a quarter of a century old, has YouTube videos showing blades stopping and retracting (flesh demonstrated by a hot dog) in fractions of a second. Injury to a digit is extremely rare and there’s little need for cut-resistant gloves. The “flesh-sensing” technology has been expanded to routers, shapers, bandsaws, and other tools where hand protection has been previously provided through gloves.

The problem, in sales-driven distribution, is that you seldom find a redefinition of product application. Distributor sellers hawk drills and gloves, they don’t talk about making holes and hand protection. A redefinition of product function doesn’t have to lead to a new product. Consulting and new service opportunities can abound from the expansion in market definition.

But, to successfully engage these revenue streams, the distributor needs a new product and/or new service introduction process. We’ve used the Stage-Gate process for many years, but there are few distributors that can show successful ongoing annual use of the funnel-based process for new income streams.

The Future of the Sales Driven Distributor

Our work in the distribution sector clearly points to declining profitability in the the sales driven culture versus marketing or operations driven cultures. Many of the sales cultures will sell out to larger firms where marketing and operating platforms are more predominant. The sales culture can succeed by reviewing their value added for what is unique and different and demonstrably advantageous to the customer. An expansion in product definition away from sales myopia is the best road out of commodity hell.

Scott Benfield is a consultant for B2B Manufacturers and Distributors. He is the author of six books and numerous research projects on B2B channels. He can be reached at benfield.scott@aol.com or (630) 640-5605.