Why This Matters to Distributors: When a competitor is compounding account penetration, wallet share and on-site technology density simultaneously in a flat market, the accounts it is winning are not coming from nowhere.

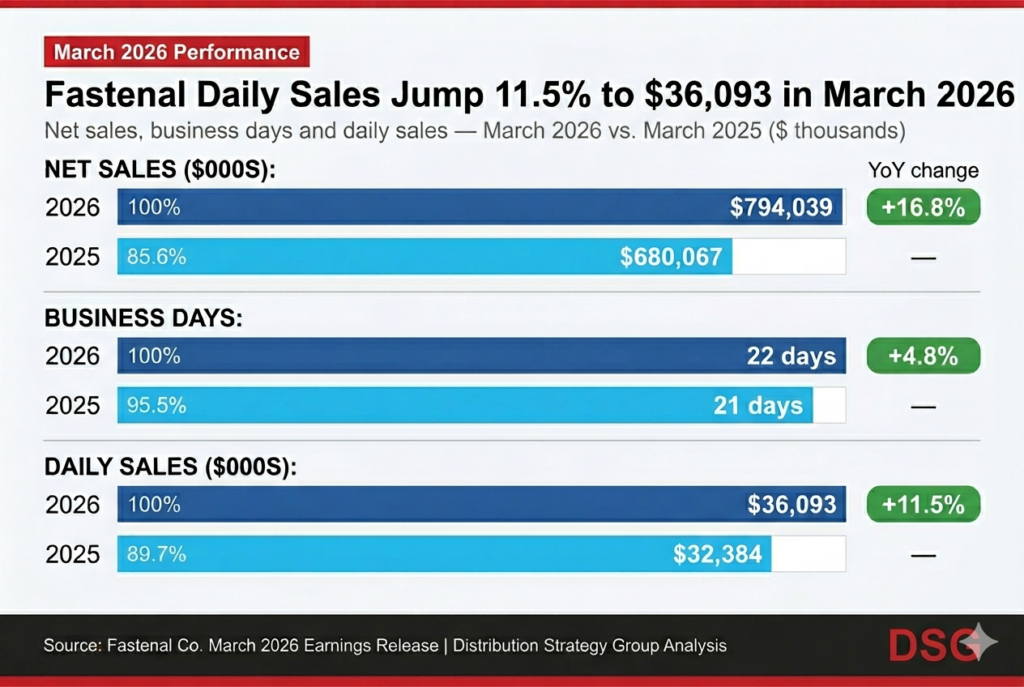

Fastenal Co. reported first-quarter 2026 daily sales growth of 12.4% to $34.9 million per day. The industrial economy gave the company almost nothing to work with. U.S. Manufacturing PMI averaged approximately 52.6% for the quarter. Demand was not broad.

“We really did not see much of a tailwind,” said Jeffery Watts, president and chief sales officer, on the company’s earnings call. “We gained share through focused execution.”

Share gain, not market expansion, is the story behind every significant data point Fastenal reported for the quarter. Non-residential construction grew 17%. Heavy manufacturing, which represents 44% of total sales, grew in the mid-teens. Non-manufacturing customer sites spending $50,000 or more per month grew 25% year over year — outpacing the company’s already strong 16% overall growth rate for that tier.

CEO Dan Floreness was direct about what the construction turnaround revealed. “It tells me a great supply chain partner is relevant to every industry out there,” he said. “We can get traction in any end market. All we have to do is understand that end market.”

International operations reinforced the breadth. Fastenal’s European and Asian businesses grew 24% in March. Watts attributed the momentum to demand for the company’s on-site model. “Our solutions, our local presence and our supply chains are definitely in high demand,” he said.

The account-level data explains the durability behind the growth rate. Customer sites spending $50,000 or more per month increased 16.3% year over year to just over 2,900 locations. Those sites now account for more than half of total company revenue. Average monthly sales by qualifying site rose $5,700. Total national account contracts grew 8% year over year to just over 3,600. Approximately 75% of Q1 revenue came from contracted customers.

Floreness described the compounding dynamic in direct terms. “We are adding customers at a very rapid pace, and we are also adding wallet share at the same time,” he said. “Our ultimate number is expanding.”

Fastenal Managed Inventory is the mechanism converting account relationships from commercial to operational. The company signed 7,000 new FMI device agreements in Q1 — approximately 110 per day, an 8% increase over the prior year. FMI-driven transactions accounted for 45% of Q1 revenue, up 150 basis points year over year. Digital channels represented 61.5% of total Q1 sales. Digital footprint daily sales grew 13.6%, outpacing overall company growth. Electronic procurement integrations accounted for 30% of total sales.

“More customers are using our on-site devices and solutions to manage inventory, which makes Fastenal a stickier and more efficient supply chain partner,” Watts said.

Gross margin was the quarter’s primary challenge. Fastenal came in approximately 50 basis points below the prior year and 40 basis points below its own internal Q1 target. Tariff-related cost increases moved through the P&L faster than pricing could recover. Floreness identified exactly where the pressure was concentrated — and where it was not. The fastener business, where Fastenal carries months of inventory visibility and direct sourcing relationships, was insulated. Branded product categories were not.

“Where we are getting squeezed is on some of those branded products, where our timeline to understanding the cost change is much different than what it is in our fastener inventory,” Floreness said. Safety products and cutting tools absorbed the bulk of the shortfall, with suppliers pushing cost increases of 6% to 8% directly through to Fastenal.

Tariff policy uncertainty extended the timeline on pricing conversations throughout the quarter. CFO Max Poneglyph described the dynamic plainly. “In many cases, customer conversations and pricing actions took longer than usual as customers worked through their own planning assumptions,” he said. “In others, these conversations were delayed as customers and suppliers await further direction on tariff changes and potential refunds.”

Fastenal realized approximately 3.5% pricing year over year, up from 3.3% in Q4 2025, but insufficient to offset cost headwinds. The company’s cumulative pricing target of 5% to 8% is unchanged. Pricing actions with effective dates ranging from March 1 through June 1 have yet to fully flow through. Poneglyph said tariff-related inventory cost headwinds are expected to clear by midyear.

Floreness was direct about the near-term outlook. “Q2 will be challenging,” he said. “I personally feel good when I look out to Q3 and Q4 because I know how long it takes to do certain things.”

Despite gross margin pressure, SG&A fell to 24.3% of sales from 25% in Q1 2025, delivering 20 basis points of operating margin expansion to 20.3%. Return on invested capital reached 31% on a trailing 12-month basis, up 180 basis points year over year. Operating cash flow was $378 million, or 111% of net income. Full-year net capital expenditure guidance of approximately $320 million remains unchanged, with investment focused on hub automation, FMI hardware, and IT infrastructure.

Floreness closed with a direct statement of competitive intent. “The economy is going to give or take what it gives or takes,” he said. “What we take from others — from a market share gains standpoint — those are pure wins.”

Do not miss any content from Distribution Strategy Group. Join our list.

Share this article: